VOO + SMH: More Tech, or Real Diversification? [2026]

Spend enough time in ETF forums and you'll see the same request on repeat: "VOO is basically half tech now, what can I add to get away from it?" And almost every time, one of the top answers is SMH. Semiconductors. It's a strange thing to recommend when you sit with it, because SMH isn't a step away from tech. It's the most concentrated tech bet on the shelf. So what actually happens when you bolt it onto VOO?

I backtested an 80% VOO / 20% SMH portfolio against plain VOO over ten years, rebalanced annually. The result is genuinely two stories at once, and keeping them separate is the whole point of this article.

This article is for educational purposes only and is not investment advice. Past performance does not guarantee future results. All figures come from historical backtests over a specific period that may not repeat.

What SMH actually is

SMH is the VanEck Semiconductor ETF. It holds around 25 companies, all in one industry: chips. NVIDIA, Broadcom, TSMC, AMD, Micron, ASML. If VOO is the entire US large-cap market in a single ticker, SMH is one narrow slice of that market, magnified.

Here's the part that matters if you already hold VOO. The biggest names in SMH are names you own. NVIDIA is about 15% of SMH and already sits at the top of VOO. Broadcom is in both. Adding SMH doesn't reach into a corner of the market VOO misses. It reaches into the corner VOO is already most exposed to and leans on it harder.

Worth clearing up the premise while we're here: VOO isn't actually 50% tech. It's roughly a third Information Technology by GICS sector, closer to 40% once you count the tech-adjacent names sitting in Communication Services. It only feels like half because nearly every top holding is a tech company. Either way, the direction is the same. Bolting semiconductors onto that isn't a hedge against tech concentration. It's more of it.

The part that complicates everything: it worked

If your instinct is to dismiss SMH as a bad idea, the data won't cooperate. Over the last decade it was the single best-performing slice of the US market, and it wasn't close.

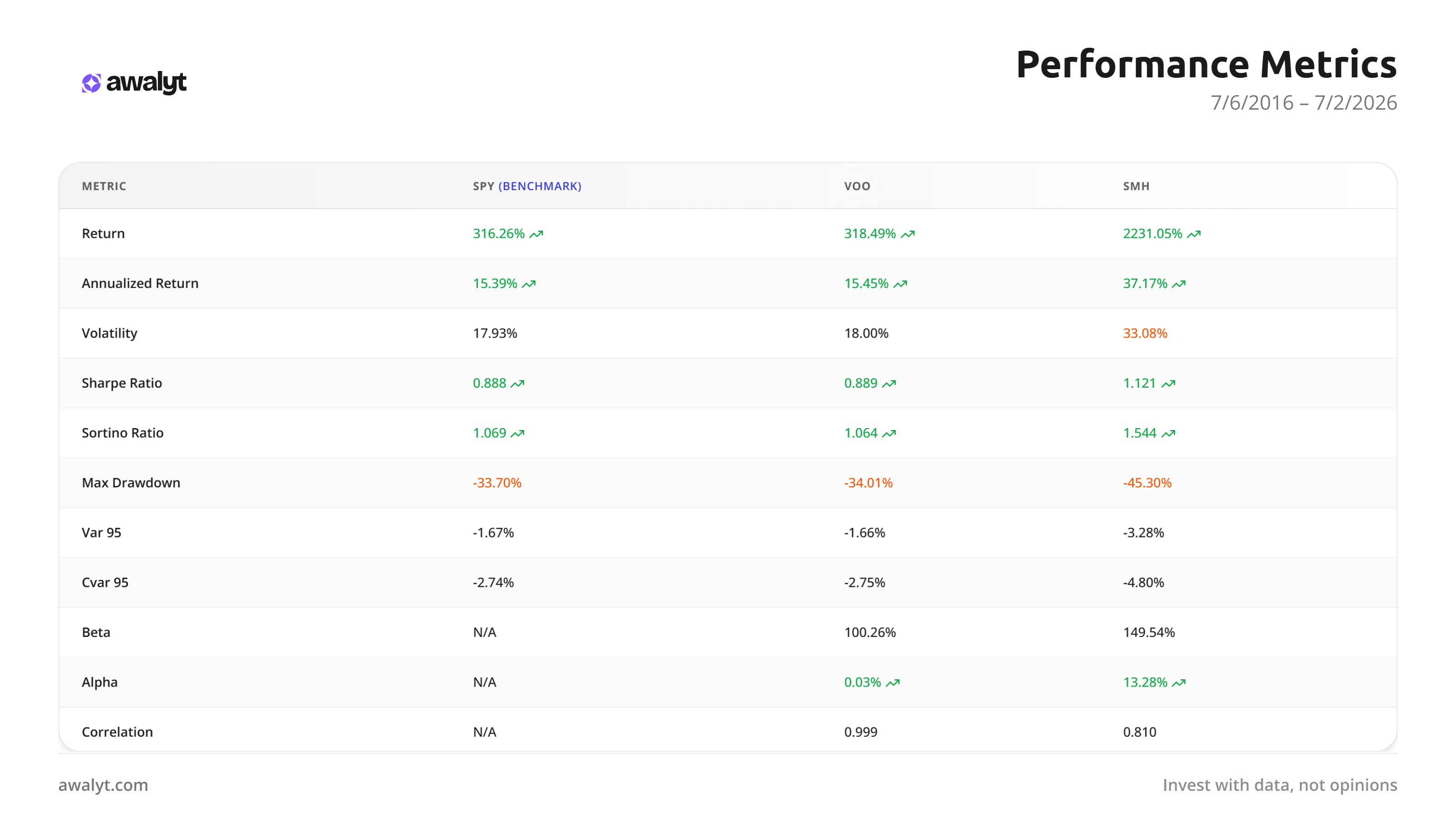

From mid-2016 to mid-2026, SMH returned 2,231% against VOO's 318%. Annualized, that's 37.17% a year versus 15.45%. It even won on a risk-adjusted basis, posting a Sharpe ratio of 1.121 against VOO's 0.889, because the returns were large enough to more than pay for the extra volatility. This wasn't one lucky year either. It was the semiconductor supercycle: cloud, then crypto, then AI, each handing the chipmakers a fresh demand story.

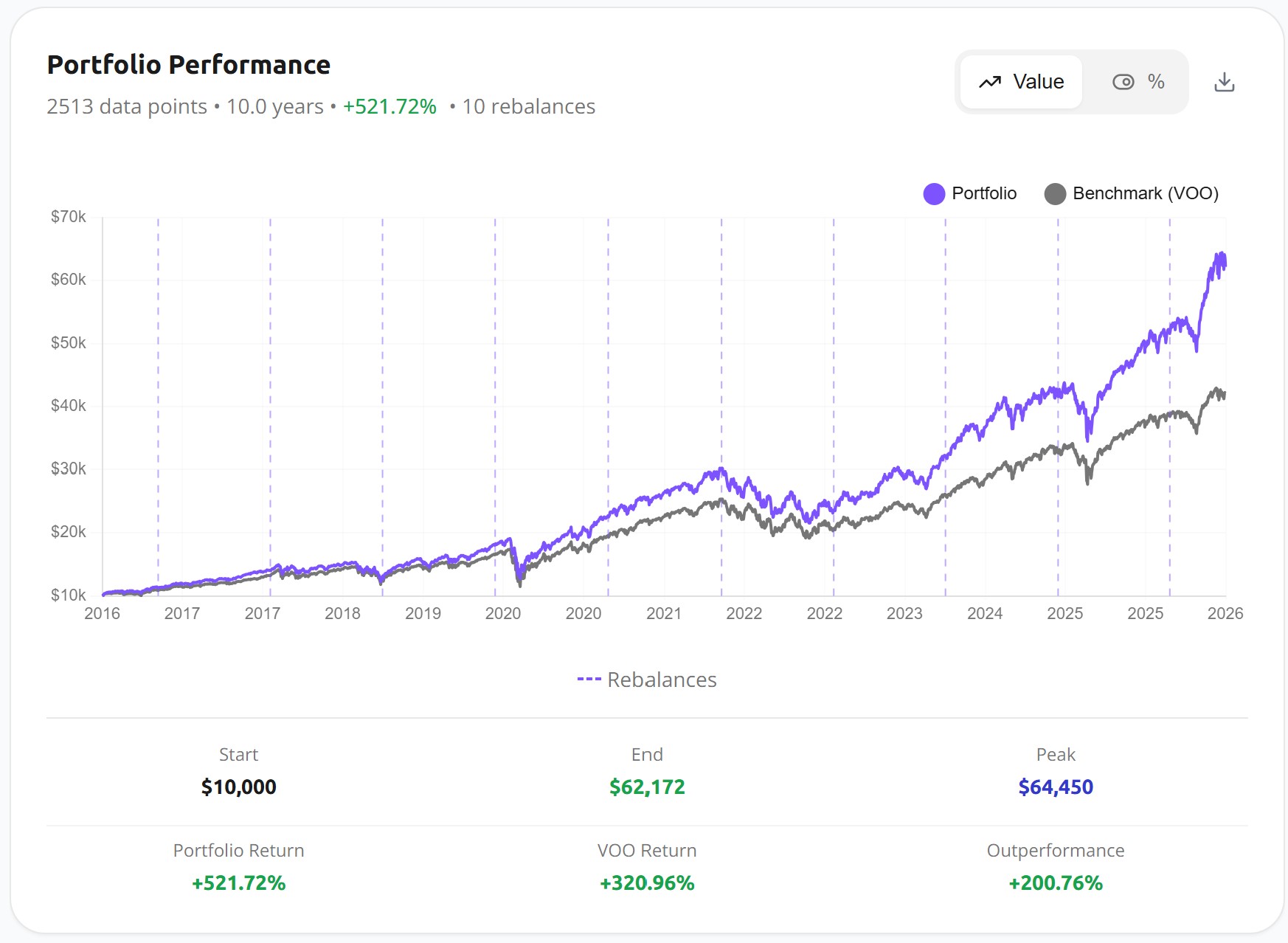

Blend 20% of that into an 80% VOO core and the sleeve carries the whole portfolio.

The 80/20 portfolio turned $10,000 into $62,172, a +521.72% total return against VOO's +320.96%. That's 200 percentage points of outperformance from a one-fifth position. It's the mirror image of the small-cap value story, where a 20% AVUV tilt barely moved the needle. Here, 20% moved almost everything.

So the tilt worked. Whether it diversified is a completely separate question, and the answer is no.

The ride underneath the return

Start with what SMH does on its own. It ran at 33% annualized volatility, nearly double VOO's 18%, with a max drawdown of -45% against VOO's -34%. At 20% of the portfolio, annual rebalancing kept most of that turbulence contained, and the blend's worst drawdown came in around -33%, essentially VOO's.

That looks reassuring, but it leans on a decade that mostly went one way. The year-by-year data shows the sleeve's teeth when the wind turned: the portfolio fell about 22% in 2022 and rode a drawdown past 33% during the 2020 crash. A fund that halves on its own doesn't stop being a fund that can halve just because you hold a fifth of it. It means the pain arrives in smaller doses, as long as the other 80% is holding up.

Why this isn't diversification

The deeper reason SMH doesn't diversify VOO is structural, and the overlap analysis makes it plain.

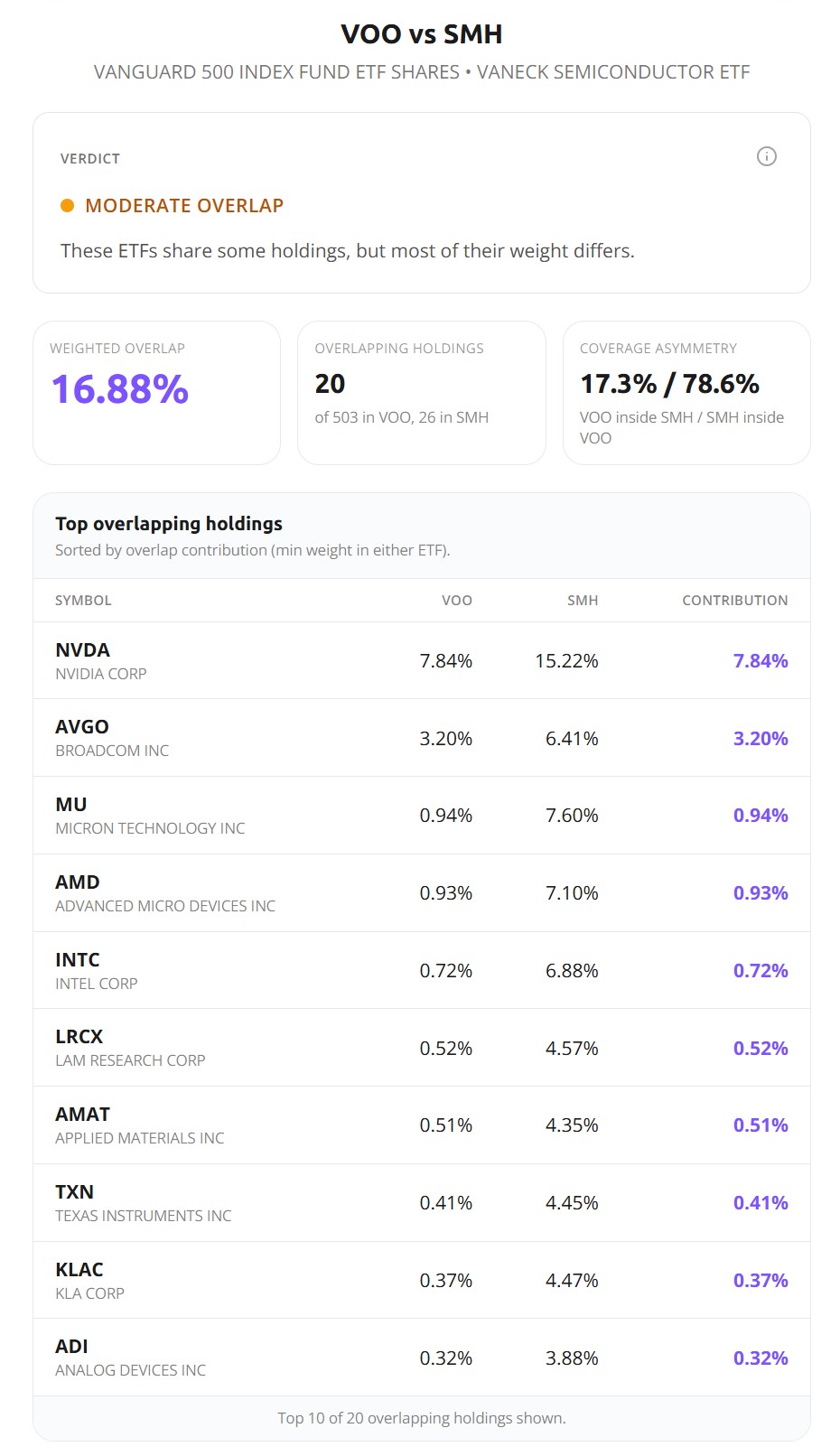

VOO and SMH share 16.88% of their weight, which sounds modest until you see where it sits. NVIDIA is the largest overlap, at 7.84% of VOO and 15.22% of SMH. Broadcom, Micron, AMD, Intel, Lam Research, Applied Materials, Texas Instruments all follow. Every one is a chip stock you already own inside VOO. The coverage asymmetry line says it cleanly: 78.6% of SMH's weight already sits inside VOO. You're not adding many new companies, you're re-buying the ones VOO holds, at higher concentration. The only genuinely new exposure is the foreign chipmakers VOO can't hold, TSMC and ASML chief among them, and that's a thin slice of what you're paying for.

Correlation confirms the structure.

Across the decade the two correlated around 0.63 on average, loose enough to pass for diversification in calm markets. But the average hides the moments that decide whether a hedge is real. When tech sold off through 2022, the correlation between VOO and SMH climbed to roughly 0.89. They fell together, hard, in the exact stretch you'd want them apart, because the thing pulling VOO down was the thing pulling SMH down: large-cap tech repricing. A second bet on the sector you're already heaviest in doesn't soften a tech drawdown. It deepens it. This is the pattern behind a lot of portfolios that look diversified on the surface and aren't, and it's the whole reason we built the correlation and overlap tools to look through the labels.

The regime you're extrapolating from

One thing deserves to be said flatly. That 37%-a-year figure is not a reasonable expectation for any equity fund. It's the record of the most explosive stretch in semiconductor history, driven by a handful of companies and, lately, by an AI buildout concentrated in NVIDIA. I aim for at least ten years in a backtest specifically so one cycle doesn't get mistaken for a permanent edge, and even ten years here captures mostly a single direction.

Semiconductors are famously cyclical. The industry has lived through peak-to-trough collapses far worse than anything in this sample, and the fund's own -45% drawdown is a mild reminder of that. Betting the next decade rhymes with the last is really a bet that the chip cycle has been repealed. Maybe it has. That's a conviction, not a base case.

So who is this actually for

Should SMH sit next to your VOO? It comes down to what you were looking for in the first place.

If you came to get away from tech, this is the wrong tool, and no reading of the data says otherwise. Adding a 100% semiconductor fund cannot reduce tech exposure. If that's the real goal, exposure VOO genuinely lacks, small-cap value or something outside US large caps does the job SMH can't.

Maybe, though, you don't want less tech at all. Maybe you want more of it, on purpose, because you think the semiconductor story has another decade left and you can sit through a fund that can cut in half. That's a coherent position, and the last ten years paid it off spectacularly. Just name it correctly. It's a concentrated, high-conviction bet on chips. Not a diversifier.

The bottom line

Adding SMH to VOO beat the index by 200 points over ten years, and made the portfolio more concentrated in the one sector it was already most exposed to, and more fragile in a tech selloff rather than less. Both are true at the same time, and holding them together is the entire lesson. "It worked" and "it diversified" are different claims, and only one of them survives the data.

If what you're actually after is exposure the S&P 500 leaves out, the place to look isn't a magnified slice of VOO's biggest bet. It's the parts of the market VOO doesn't hold at all, which is a different article, and the one worth reading next.

Want to test these insights on your own portfolios?

Awalyt is a portfolio analysis platform: backtesting on daily data, fundamental analysis, asset analysis, and AI-powered insights.

Get Started Free