Nike Stock: Turnaround or Value Trap? What the Data Shows Before Q3 Earnings [March 2026]

Nike reports its Q3 FY2026 earnings on March 31, 2026, after the market close. The stock is trading near $65 — its lowest level in almost a decade — down roughly 24% over the past year.

Unlike some beaten-down stocks where the price drops while the business keeps growing, Nike's situation is different. Revenue is declining, margins are compressing, and net income has dropped significantly. The numbers confirm that something real is happening here, not just a sentiment-driven selloff.

But there's also a new chapter being written. CEO Elliott Hill, a 32-year Nike veteran, is leading an aggressive turnaround strategy called "Win Now." Early signs in North America are encouraging. The question is whether those signs will spread to the rest of the business — or fade.

In this analysis, we use Awalyt's fundamental analysis tools to break down what the data actually shows, what's improving, what's still deteriorating, and what investors should watch on March 31.

Disclaimer: This article is for educational and informational purposes only. It does not constitute investment advice. Always do your own research before making any investment decisions.

The Big Picture: A Giant Under Pressure

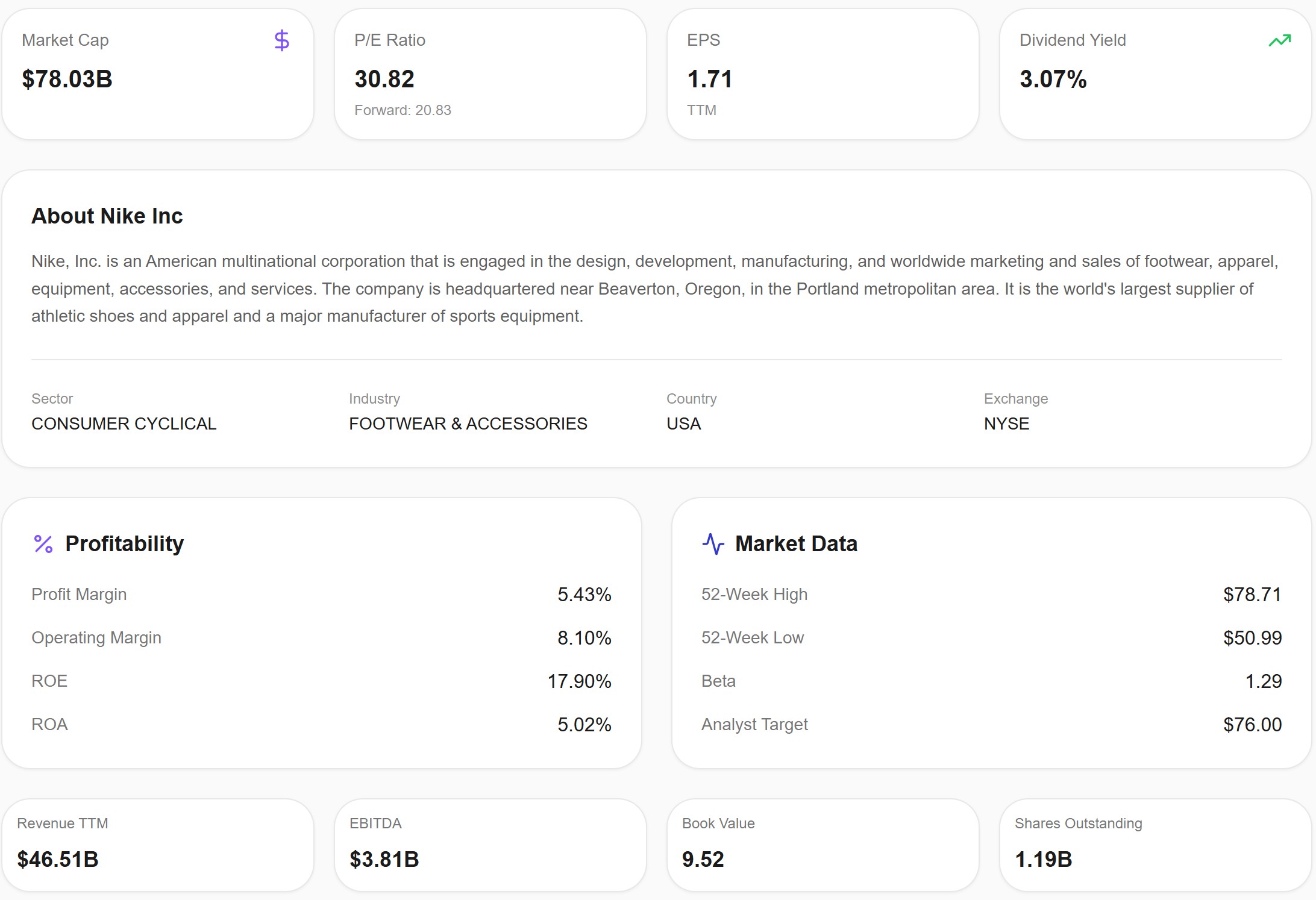

Nike is the world's largest athletic footwear and apparel company, with trailing twelve-month revenue of $46.5 billion. It's a Dow Jones component, a globally recognized brand, and a company that has historically rewarded long-term shareholders with consistent growth and dividends.

But the last two years have been difficult. Under former CEO John Donahoe, Nike pursued an aggressive direct-to-consumer (DTC) strategy that pulled the brand away from wholesale partners like Foot Locker and Dick's Sporting Goods. The idea was to sell more through Nike.com and Nike stores, capturing higher margins. Instead, the strategy backfired: Nike lost shelf space to competitors like On Running, Hoka, and a resurgent Adidas, while its own digital sales couldn't fill the gap.

Here's the snapshot: a $78 billion market cap (down from $190B+ at the peak), a trailing P/E of about 30.8x, EPS of $1.71, and a dividend yield of 3.07%. Profit margin sits at just 5.4% and operating margin at 8.1% — both well below Nike's historical norms.

Elliott Hill took over as CEO in October 2024 and immediately began reversing course. He's rebuilding wholesale relationships, refocusing on sport-driven product innovation, and cutting costs. Fiscal 2026 is what he calls a "transition year" — the hard reset before, hopefully, a return to growth.

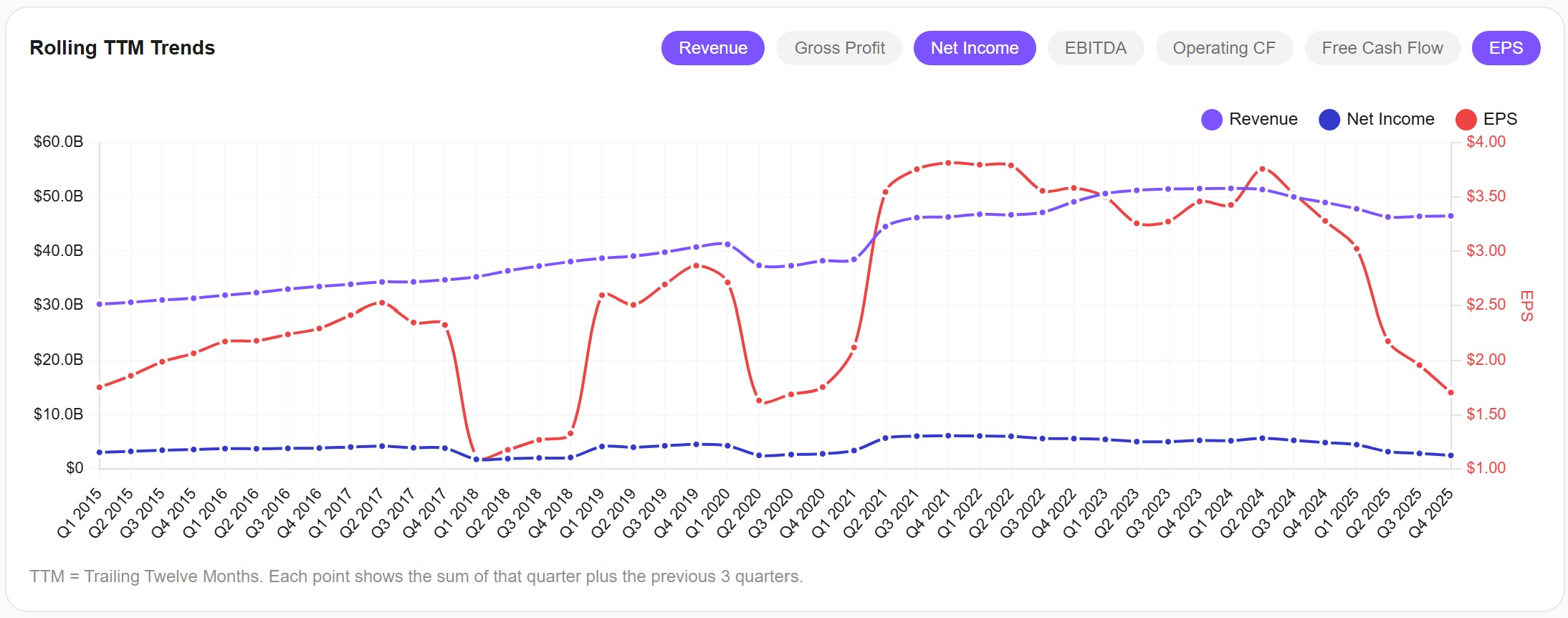

Revenue, Earnings, and EPS: The Decline Is Real

This chart tells the story clearly. Revenue peaked at around $53 billion in TTM terms and has declined to approximately $46.5 billion. Net income and EPS have fallen even more sharply — EPS dropped from roughly $3.75 at its peak to $1.71 today.

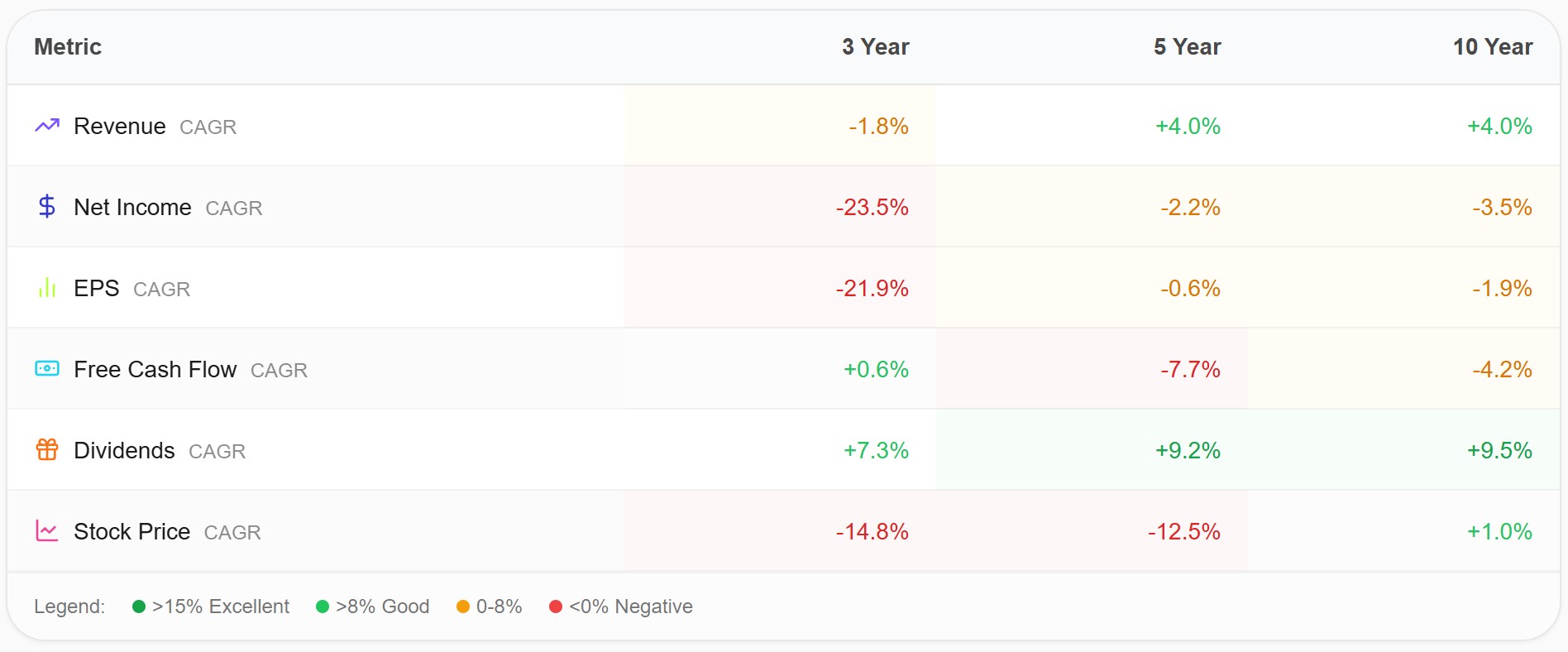

The growth table makes the magnitude of the decline explicit:

Over the last three years, revenue has declined at -1.8% annually, net income at -23.5%, and EPS at -21.9%. On a 5-year and 10-year basis, the numbers are only marginally better — even the 10-year revenue CAGR is just 4%, which is modest for a company of Nike's scale and brand power.

The one bright spot is dividends: Nike has continued to raise its dividend consistently, with a 10-year CAGR of 9.5%. The current yield of 3.07% is among the highest in Nike's history, reflecting how far the stock price has fallen rather than any acceleration in payouts.

Stock price CAGR tells the full story of shareholder pain: -14.8% over 3 years, -12.5% over 5 years. A decade of holding Nike stock has returned roughly 1% annually — barely keeping up with inflation.

For Q3 FY2026 specifically, Wall Street consensus expects revenue of approximately $11.2 billion (down low single digits year-over-year) and EPS of roughly $0.30. Nike's own guidance suggests modest growth in North America but continued headwinds in Greater China and Converse.

It's worth noting that in Q2, Nike surprised positively: EPS came in at $0.53 versus the $0.37 consensus, a 43% beat. North America revenue grew 9%, and wholesale was up 8% overall. Those are the first tangible proof points for the turnaround.

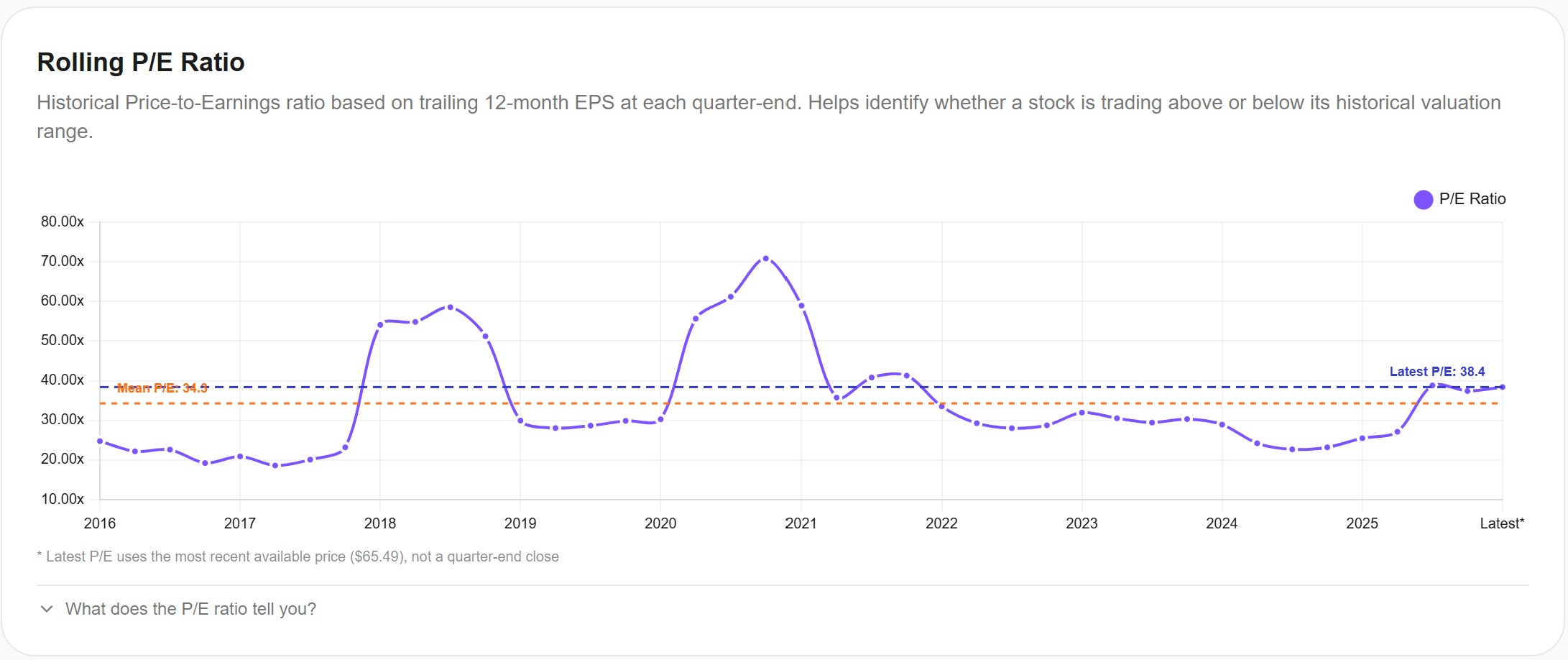

Valuation: Expensive for a Declining Business, Cheap for a Recovery

Nike's trailing P/E currently sits at around 38x, with a 10-year mean of about 35x. At first glance, this doesn't look cheap — and it isn't, on a trailing basis. Nike's earnings have compressed significantly, so the P/E is elevated not because the price is high, but because earnings are low.

The forward P/E of approximately 21x tells a different story. If analysts are right about the earnings recovery trajectory, Nike starts to look more reasonably valued on a forward basis. The analyst consensus price target is $76 — about 17% above the current price.

This is where the "turnaround or value trap" question becomes real. If earnings recover to their 2022-2023 levels (EPS around $3.00-3.75), today's price represents a P/E of roughly 17-22x — which would be among the cheapest valuations Nike has seen in a decade. But if the turnaround stalls and EPS stays near $1.71, the stock is trading at over 38x — expensive for a business in decline.

The investment case for Nike today is fundamentally a bet on the direction of earnings, not on the current valuation.

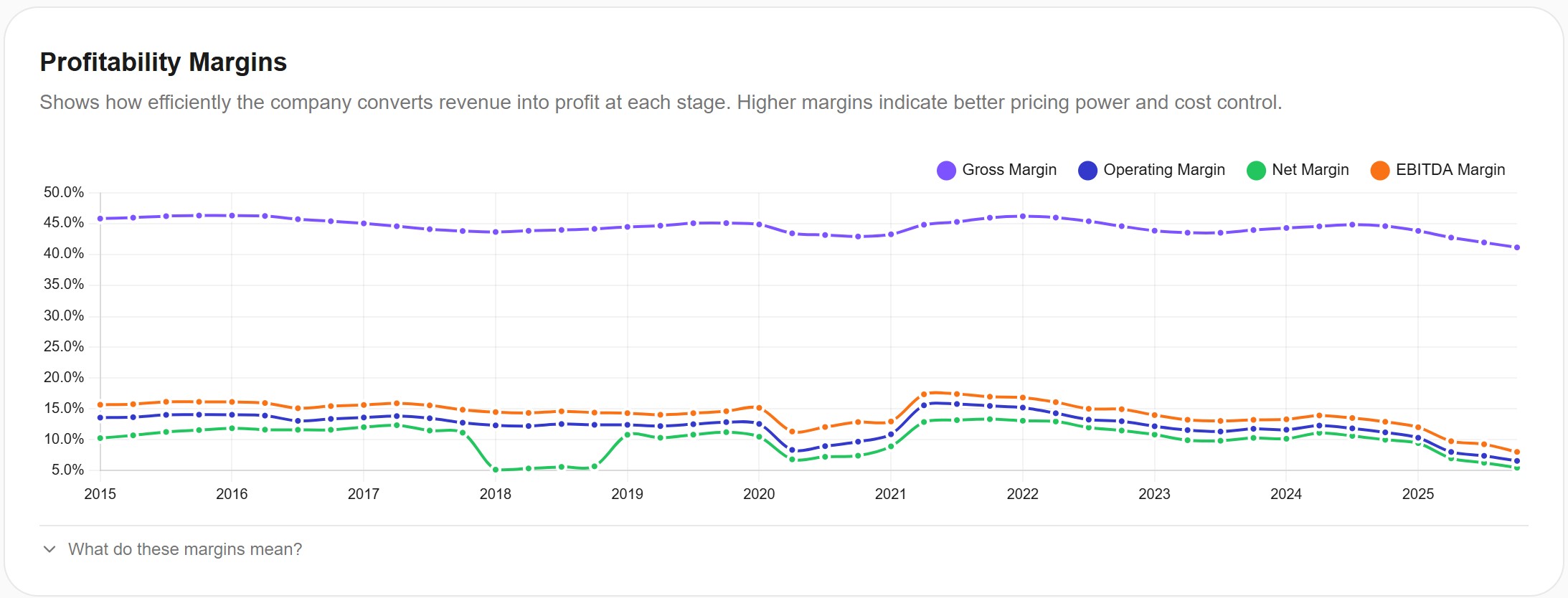

Profitability: Margins Under Significant Pressure

The profitability chart is where the pain is most visible. Gross margins have declined from their historical range of 44-46% to approximately 41%. Operating margins have dropped from 13-14% to about 8%. Net margins have compressed from 10-12% to roughly 5%.

This compression is driven by multiple factors working simultaneously against Nike: heavy discounting to clear excess inventory built up during the DTC push, higher promotional activity to compete with brands like On Running and Hoka that are gaining market share, approximately $1.5 billion in annualized tariff costs that are directly hitting cost of goods sold, and the ongoing reset of classic franchises (Air Force 1, Jordan 1, Dunk) which created a $550 million revenue headwind in Q2.

Management has guided Q3 gross margins to decline an additional 175-225 basis points year-over-year. However, they've also noted that excluding the tariff impact (about 315 basis points), gross margins would actually be expanding. This distinction matters: it suggests that the underlying business is improving, but the tariff headwind is masking the progress.

If tariffs ease or Nike successfully offsets them through sourcing shifts (moving production from China to Vietnam, which is already underway) and selective price increases, the margin recovery could be faster than the market expects.

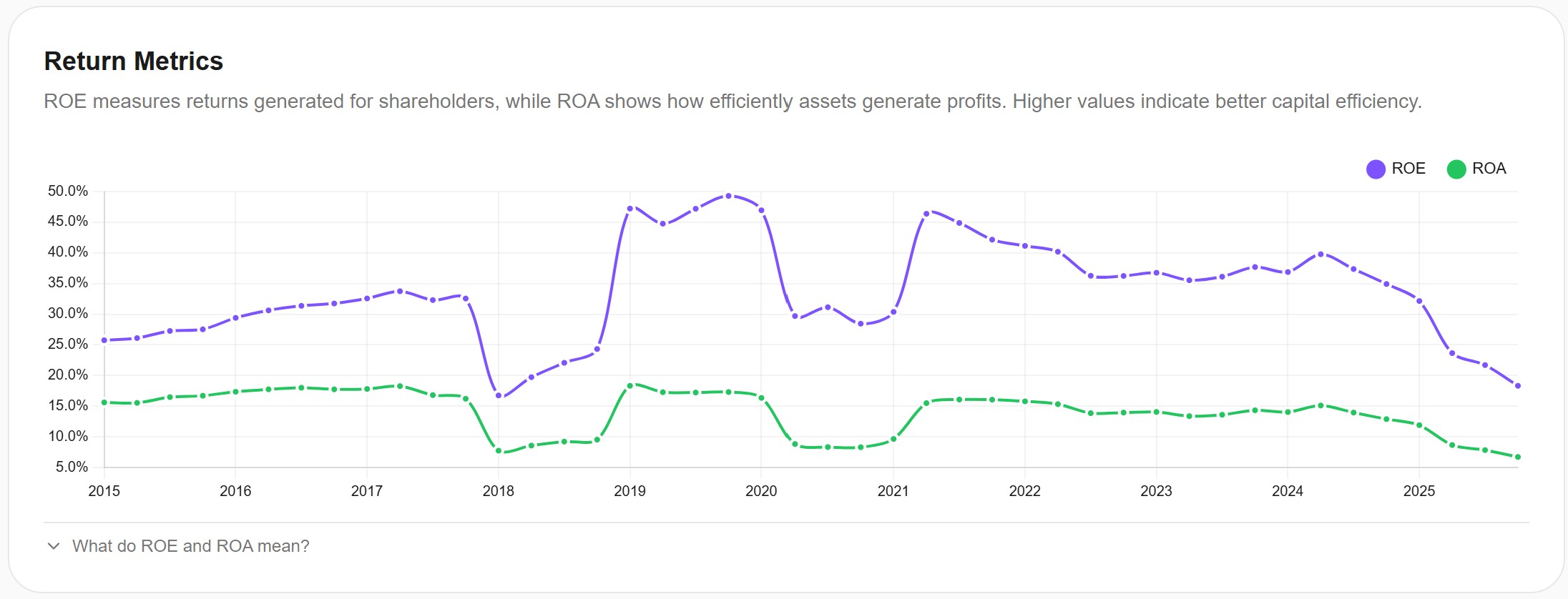

Return on Capital: Falling to Multi-Year Lows

ROE has dropped from approximately 40% (in 2024) to about 18%, while ROA has fallen from 13% to roughly 5%. Both metrics are at or near their lowest levels in a decade.

This is the clearest quantitative evidence that Nike's profitability engine has deteriorated meaningfully. For context, a 17.9% ROE is still respectable for a consumer company, but it's a far cry from the 40-50% levels that once made Nike one of the most capital-efficient businesses in the world.

The direction of ROE over the next few quarters will be one of the most important signals for whether the turnaround is gaining traction or stalling.

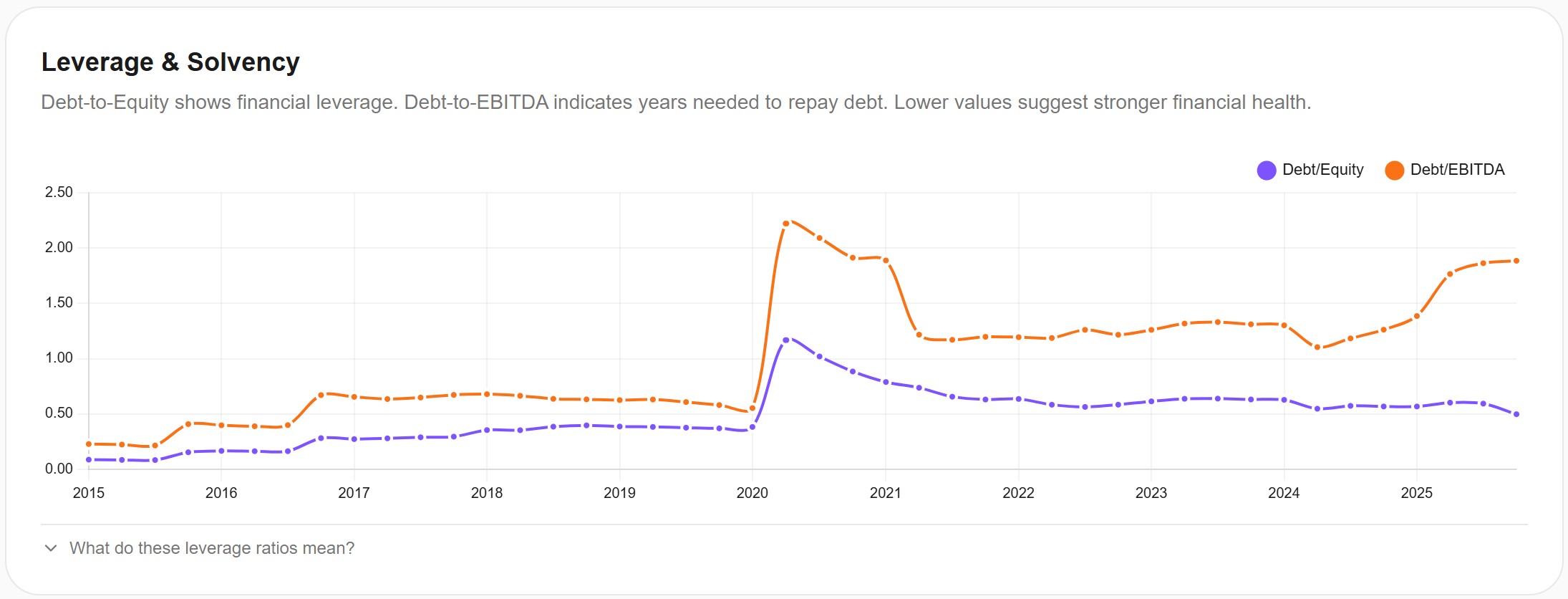

Leverage: Manageable but Trending the Wrong Way

Nike's debt-to-equity ratio sits at approximately 0.5x — reasonable and well within manageable territory. However, debt-to-EBITDA has risen to about 1.9x, up from under 1x in prior years. This increase is driven by the decline in EBITDA rather than an increase in debt, but it's worth monitoring.

Nike's balance sheet is not a concern today. The company has investment-grade credit ratings and ample liquidity. But the leverage trend reinforces the broader picture: profitability is declining, and that affects every ratio in the financial profile.

One positive: Nike continues to pay and raise its dividend, and the 3.07% yield provides some income cushion for patient shareholders. The company has raised its dividend for over 20 consecutive years.

The Turnaround: Elliott Hill's "Win Now" Strategy

This is the heart of the Nike story right now. Elliott Hill, who spent 32 years at Nike before briefly retiring, returned as CEO in October 2024 with a clear mandate: fix what his predecessor broke.

His "Win Now" strategy operates across five pillars: culture, product, marketing, marketplace, and in-person experiences. Here's what's actually happening on the ground.

Wholesale rebuild. Hill immediately began repairing relationships with the retail partners that Donahoe had alienated. Nike has rejoined Amazon (after exiting in 2019), deepened its partnerships with Foot Locker and Dick's Sporting Goods, and shifted focus back to wholesale distribution. The results are already visible: wholesale revenue grew 8% in Q2 FY2026, with North America wholesale up 24%. This is the most tangible proof that the strategy is working.

Product innovation. After years of criticism that Nike was coasting on legacy franchises like Air Force 1 and Dunks, Hill's team has unveiled several new product platforms: Nike Mind (neuroscience-driven sneaker design), Project Amplify (bionic-powered footwear), Aero-FIT cooling fabric, and Therma-FIT Air Milano temperature-regulating apparel. The running category has grown over 20% for two consecutive quarters.

Marketing investment. Nike is spending over $5 billion on marketing in fiscal 2026, shifting from promotional, price-driven tactics to brand-building storytelling. Major pushes are planned around the 2026 FIFA World Cup and other global sporting events.

Organizational restructuring. Hill flattened the leadership structure, eliminated the Chief Technology Officer and Chief Commercial Officer roles, realigned approximately 8,000 employees around sport-specific categories (running, basketball, football, training), and appointed a new COO to integrate technology into operations. This has also meant workforce reductions: 775 distribution center jobs were cut in January 2026, adding to approximately 1,000 corporate positions eliminated in 2025.

The classics reset. Revenue from oversaturated franchises (Air Force 1, Jordan 1, Dunk) declined 20% in Q2, creating a near-term headwind but clearing the path for healthier, full-price selling in the future.

Key Risks to Monitor

The Nike turnaround is not guaranteed, and the data shows several areas of genuine concern.

1. Greater China remains a significant drag. Revenue in Greater China declined 16-17% in Q2 FY2026. Nike faces intense local competition from brands like Anta and Li Ning, combined with broader economic softness in the region. Hill has acknowledged that China requires a longer timeline and a distinct approach.

2. The competitive landscape has shifted. On Running, Hoka (owned by Deckers), and a resurgent Adidas have captured market share that Nike ceded during the DTC era. Rebuilding wholesale relationships takes time, and retailers who gave Nike's shelf space to competitors won't simply hand it back. Morgan Stanley recently noted that some of these share losses may be structural rather than cyclical.

3. Tariff costs are substantial. Nike faces approximately $1.5 billion in annualized tariff costs that are compressing margins. While the company is mitigating through sourcing diversification (shifting production from China to Vietnam) and selective price increases, this remains a meaningful headwind that is largely outside Nike's control.

4. Converse is in freefall. Converse revenue dropped 30% year-over-year in Q2 FY2026. This isn't just a business cycle issue — it suggests a brand relevance problem that may require a fundamentally different approach.

5. Execution risk on the turnaround itself. Hill is simultaneously cutting costs, restructuring leadership, rebuilding wholesale, innovating on product, and investing in marketing. Doing all of this at once while managing a $46 billion revenue business is extraordinarily complex. As Needham analysts noted after Q2 results, the company's issues were "far deeper" than initially realized.

What to Watch on March 31

When Nike reports Q3 FY2026 earnings, these are the metrics that matter most.

North America revenue growth. This is the region where the turnaround is most advanced. Continued mid-to-high single digit growth would validate the wholesale rebuild strategy and serve as a blueprint for other regions.

Wholesale revenue trend. The 8% growth in Q2 was the strongest signal of progress. Investors need to see this momentum sustained or accelerating.

Gross margin trajectory. Guidance is for a 175-225 basis point decline. Any performance better than guidance — especially excluding tariff impact — would suggest the underlying business is healthier than the headline numbers show.

Greater China performance. A deceleration in the rate of decline would be encouraging. Continued -15%+ declines would raise questions about how long the China headwind will persist.

Classic franchise revenue. The -20% decline in Q2 was intentional (reducing supply of oversaturated products). Investors should look for signs that this headwind is peaking and that newer products are starting to fill the gap.

Forward guidance. Any commentary on the trajectory for Q4 and into FY2027 will be critical for determining whether the market starts pricing in a recovery or continues to discount the stock.

The Bottom Line

Nike's situation is fundamentally different from companies that are simply undervalued on strong fundamentals. The data shows real deterioration: declining revenue, compressing margins, falling returns on capital, and a stock price that has gone essentially nowhere in a decade.

At the same time, there are genuine early signs that Elliott Hill's turnaround strategy is gaining traction. North America is growing again, wholesale relationships are being rebuilt, the product pipeline is more innovative than it's been in years, and the company is investing heavily in brand-building. The Q2 earnings surprise — beating EPS estimates by 43% — suggests the market's expectations may be too pessimistic.

The honest assessment is that Nike today is neither a clear buy nor a clear avoid. It's a show-me story. The brand remains one of the most powerful in the world, with distribution scale and marketing firepower that no competitor can match. But the financials need to prove that the turnaround is real and sustainable, not just a favorable comparison against weak prior-year numbers.

For investors, the March 31 earnings report is a key checkpoint. Not the final answer — turnarounds take years, not quarters — but an important data point on whether the trajectory is heading in the right direction.

All fundamental data and charts in this article were generated using Awalyt's fundamental analysis tools. Awalyt provides institutional-grade financial analysis with daily data granularity — including profitability ratios, valuation metrics, growth trends, and more — for investors who want to see beyond the headlines.

Want to test these insights on your own portfolios?

Awalyt is a portfolio analysis platform: backtesting on daily data, fundamental analysis, asset analysis, and AI-powered insights.

Get Started FreeRelated Insights

Is Adobe the Most Undervalued Tech Stock Right Now? A Data-Driven Analysis [March 2026]

14 min read

How to Tell If a Stock Is Overvalued or Undervalued: A Framework with Real Examples [2026]

13 min read

How to Use Historical P/E to Tell If a Stock Is Cheap or Expensive [2026]

10 min read