Is Adobe the Most Undervalued Tech Stock Right Now? A Data-Driven Analysis [March 2026]

Adobe reports its Q1 FY2026 earnings on March 12, 2026, after the market close. The stock is down roughly 35% over the past year and trading near its lowest P/E multiple in a decade. Meanwhile, the business keeps posting record revenue and expanding cash flow.

So what's going on? Is the market right to punish Adobe, or are the fundamentals telling a different story?

In this analysis, we break down Adobe's key financial metrics using Awalyt's fundamental analysis tools — from valuation and profitability to cash flow generation and growth trends — to help you form your own view ahead of the earnings release.

Disclaimer: This article is for educational and informational purposes only. It does not constitute investment advice. Always do your own research before making any investment decisions.

The Big Picture: What You Need to Know

Before we dig into the numbers, here's the context that matters.

Adobe is the dominant player in creative software (Photoshop, Illustrator, Premiere Pro), document management (Acrobat, PDF), and digital marketing (Experience Cloud). It generates nearly all of its revenue through subscriptions, with annual recurring revenue (ARR) reaching $25.2 billion at the end of FY2025 — up 11.5% year-over-year.

Despite posting record revenue of $23.77 billion in FY2025 and generating over $10 billion in operating cash flow, the stock has been in a sustained downtrend. The primary concern? That generative AI tools from competitors like Canva, Midjourney, OpenAI, and Figma could erode Adobe's market position and pricing power over time.

This is the tension at the heart of the Adobe investment case right now: exceptional fundamentals versus existential narrative risk.

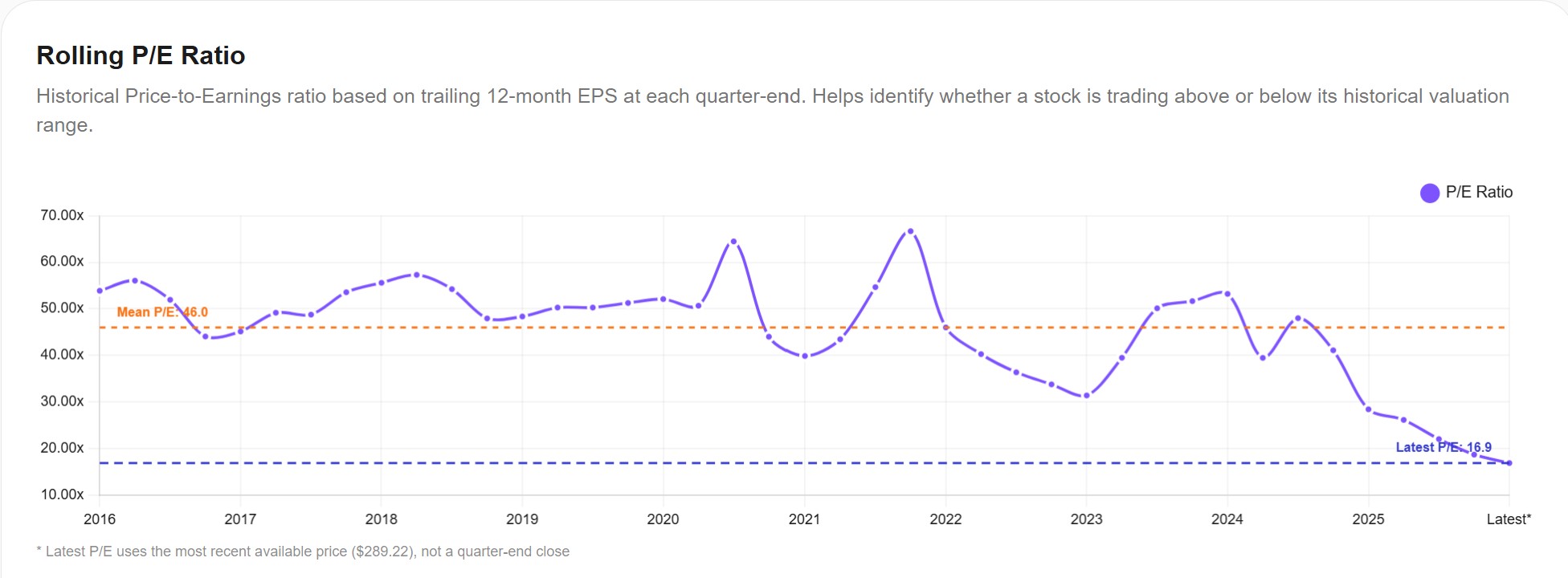

Valuation: The Cheapest Adobe Has Been in a Decade

Let's start with the most striking data point.

Adobe's trailing P/E ratio currently sits at approximately 16.9x, against a 10-year historical average of 46x. The forward P/E (based on FY2026 earnings estimates) is around 12x.

To put this in perspective, Adobe has not traded at these multiples since before it completed its transition to subscriptions in the mid-2010s. Here are some useful comparison points:

- The S&P 500 currently trades at roughly 20-21x earnings

- Microsoft trades at about 28-30x

- Salesforce trades at around 25x

- The broader software sector averages approximately 27x

Adobe is trading at a significant discount not just to its own history, but to virtually every comparable software peer. The market is pricing the stock as if growth is about to stall — something the actual numbers haven't shown yet.

Morningstar currently estimates Adobe's fair value at $516, implying roughly 80% upside from current levels. The average analyst price target sits around $415, suggesting about 46% upside.

Of course, a cheap stock can always get cheaper. Valuation alone is never a buy signal. But it does set the stage for the rest of the analysis: are the fundamentals deteriorating, or is this a sentiment-driven selloff?

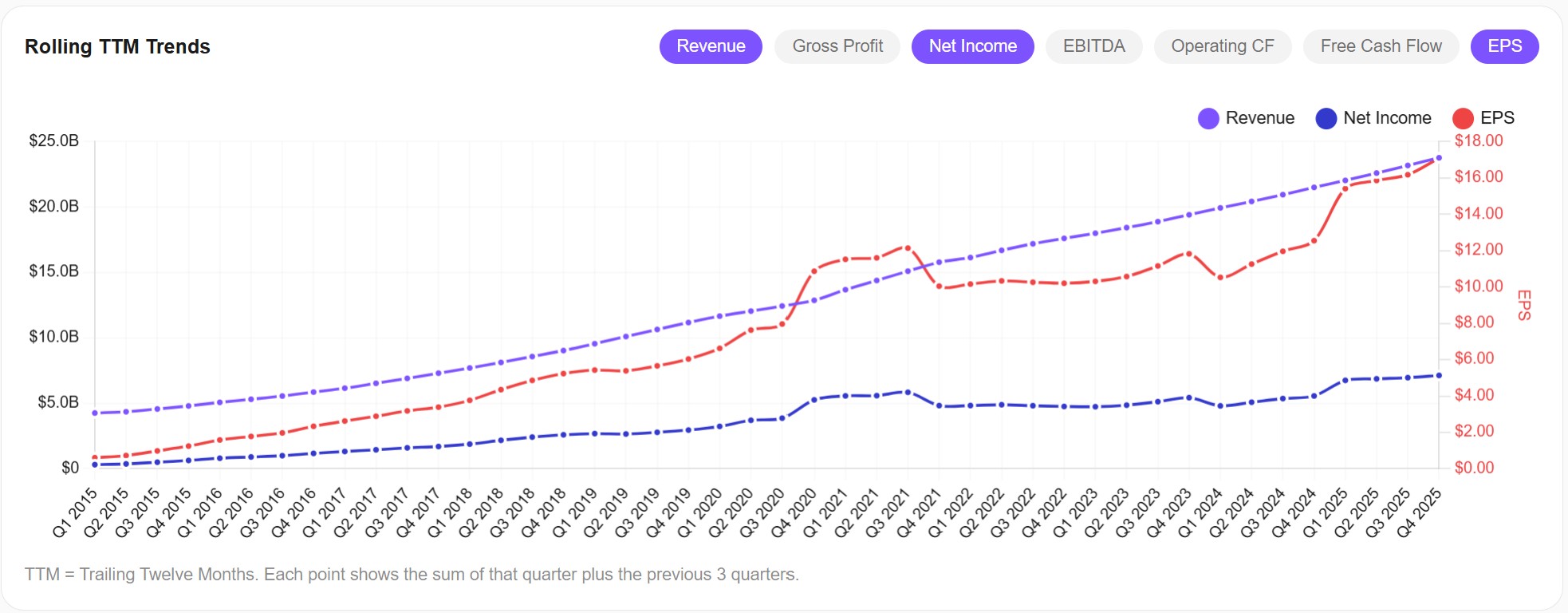

Revenue, Earnings, and EPS: The Growth Engine

Looking at Adobe's rolling trailing-twelve-month (TTM) trends, the picture is clear: consistent, compounding growth across revenue, net income, and earnings per share over the past decade, with no visible inflection downward.

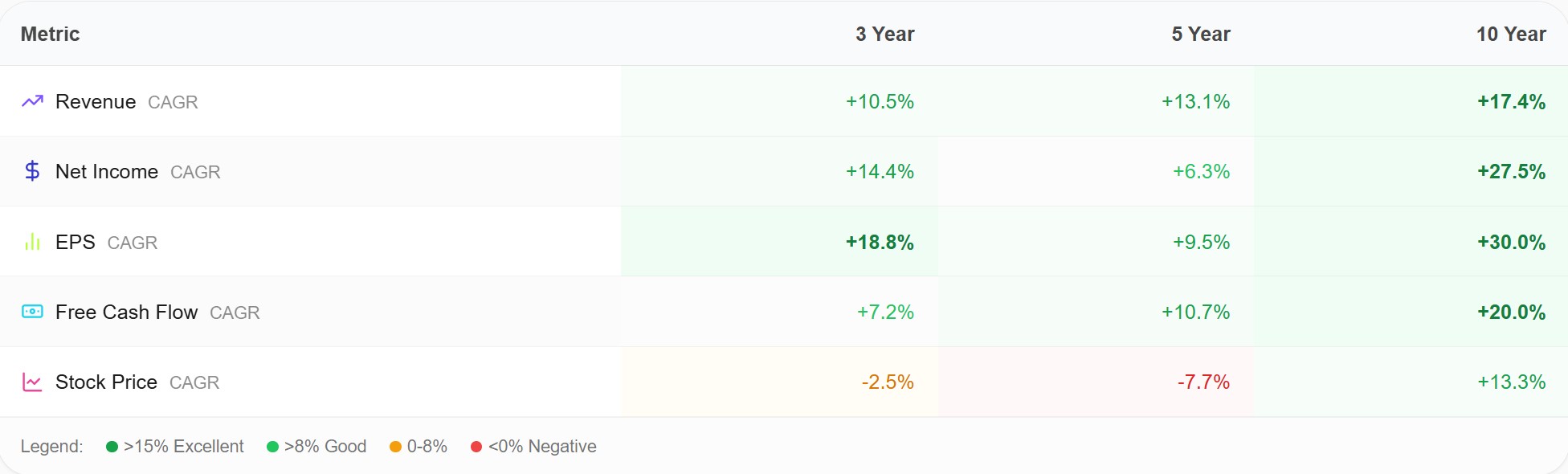

The growth table makes this even more explicit:

Over the last three years, Adobe has compounded revenue at 10.5% annually, EPS at 18.8%, and free cash flow at 7.2%. On a 10-year basis, the numbers are even more impressive: revenue CAGR of 17.4% and EPS CAGR of 30%.

But look at the bottom row: stock price CAGR is -2.5% over 3 years and -7.7% over 5 years. The business has grown significantly while the stock has gone nowhere (or down). This kind of divergence between fundamentals and price doesn't happen often in large-cap tech stocks, and it typically resolves — one way or the other.

For Q1 FY2026 specifically, Wall Street consensus expects:

- Revenue: approximately $6.28 billion (+10% year-over-year)

- EPS: approximately $5.87–5.88 (+15.5% year-over-year)

- Digital Media ARR: approximately $19.44 billion (up from $17.63 billion a year ago)

Adobe's own guidance is for $6.25–6.30 billion in revenue and $5.85–5.90 in non-GAAP EPS. The company has beaten consensus estimates in each of its last four quarters.

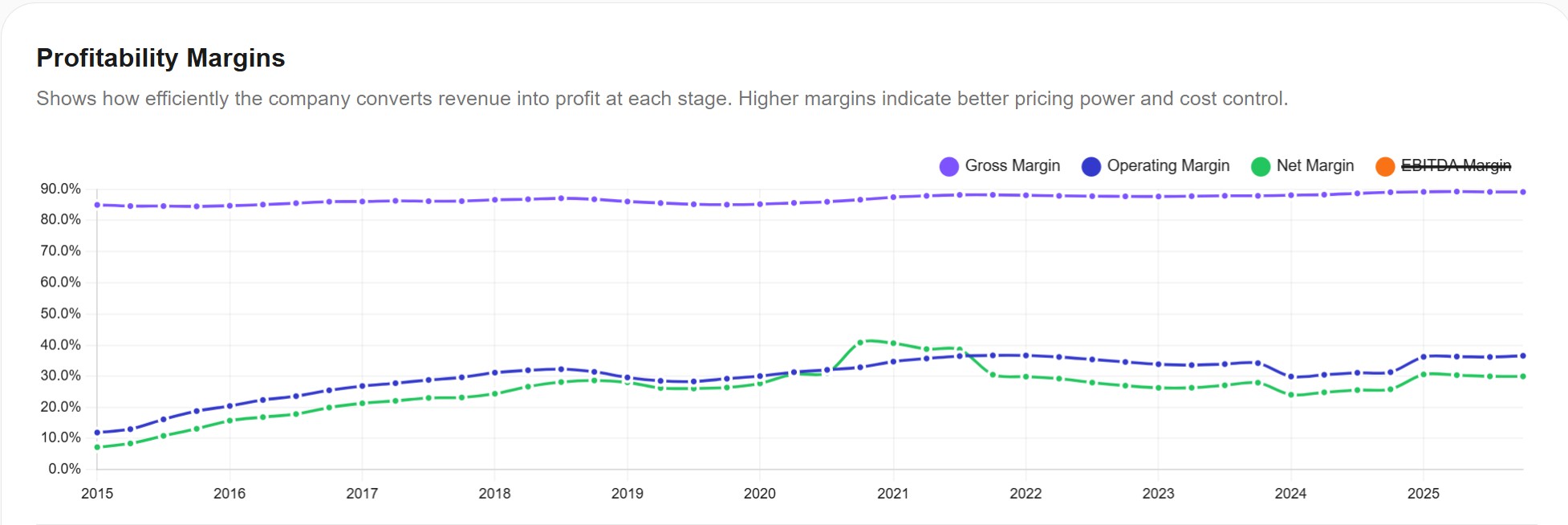

Profitability: A Cash-Generating Machine

Adobe's margin profile is one of the strongest in the entire software industry:

- Gross margin: approximately 88%, stable and among the highest of any public software company

- Operating margin: approximately 36.5%, with a clear upward trajectory since 2015

- Net margin: 30%, which is exceptional for a company at this scale

These aren't just good numbers — they reflect a business with enormous pricing power and operating leverage. Software companies with gross margins near 90% have very high incremental margins on every additional dollar of revenue, which is why Adobe has been able to grow earnings faster than revenue over time.

The profitability chart from Awalyt shows that margins have been remarkably stable despite the competitive noise around AI. If Canva and other tools were truly eating into Adobe's business, you'd expect to see margin compression — especially in gross margins, as Adobe would need to invest heavily in AI compute or cut prices. That hasn't happened yet.

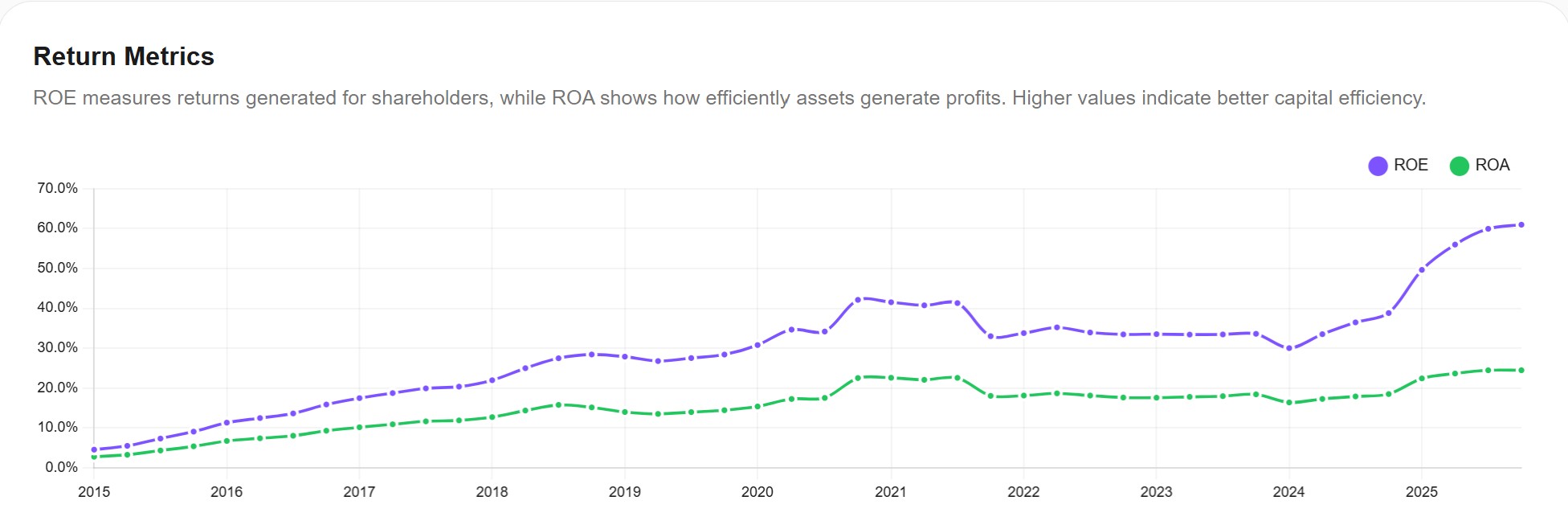

Return on Capital: Reaching New Highs

Adobe's return on equity (ROE) has surged to approximately 55–60% in the most recent quarters, while return on assets (ROA) stands around 18–23%. Both metrics are at or near all-time highs.

High and rising ROE tells you that the company is becoming more efficient at generating profits from shareholders' capital. Combined with moderate leverage (more on that below), this paints a picture of a business that is getting better at deploying capital, not worse.

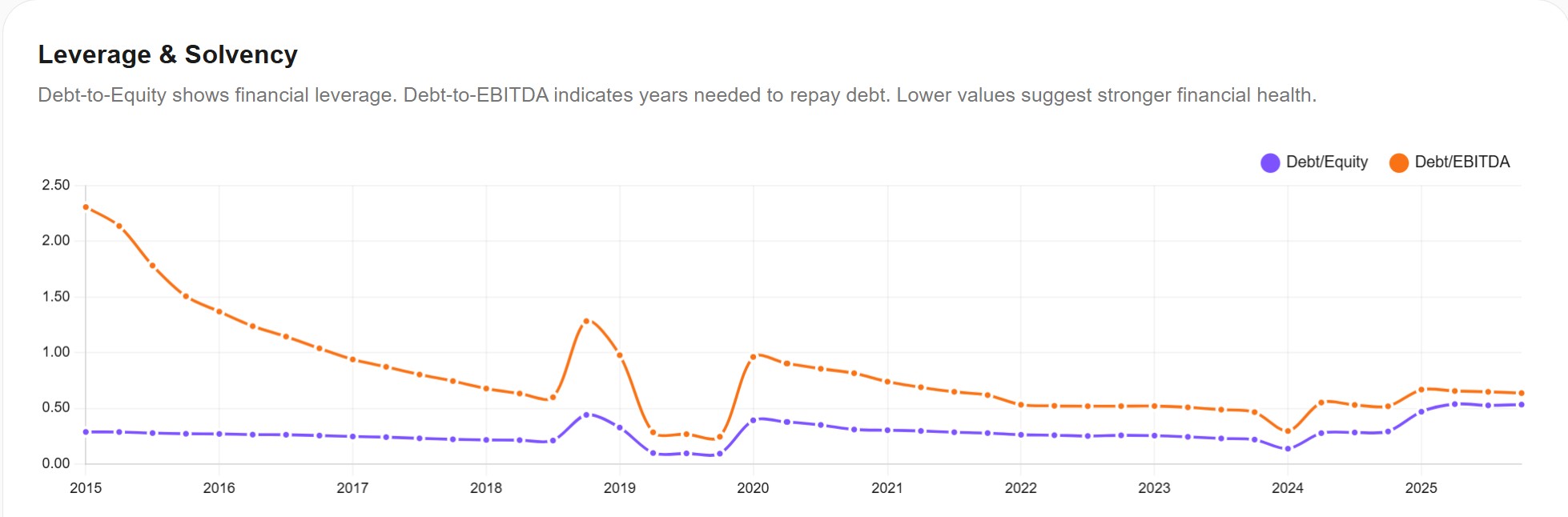

Leverage and Financial Health: Conservative Balance Sheet

Adobe runs a conservative balance sheet. The debt-to-equity ratio sits at roughly 0.55x, and debt-to-EBITDA is approximately 0.6x — both well below levels that would cause concern. The long-term trend shows dramatic deleveraging from the 2015 era (when Debt/EBITDA was above 2x).

This matters because Adobe has significant financial flexibility. With over $10 billion in annual operating cash flow and minimal debt obligations, the company can simultaneously fund R&D, pursue acquisitions, and return cash to shareholders without stress.

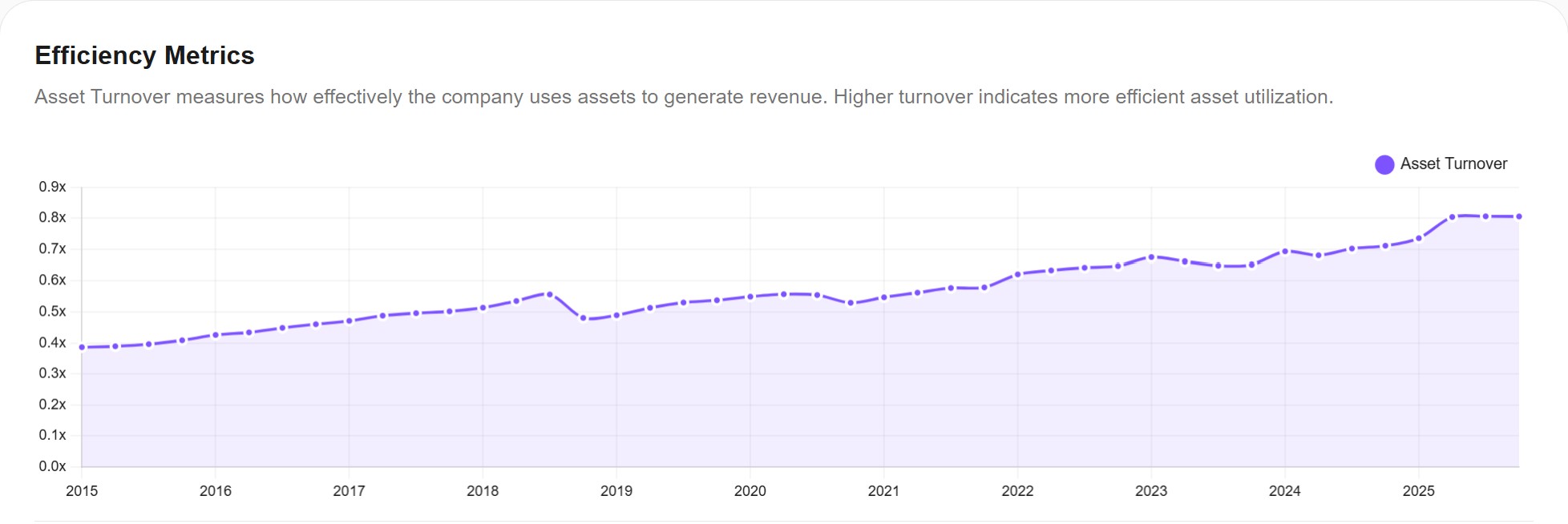

Efficiency: Getting More From Every Dollar

Asset turnover has roughly doubled over the past decade, rising from 0.4x in 2015 to approximately 0.8x today. This means Adobe is generating nearly twice as much revenue per dollar of assets as it did a decade ago — a sign of operational efficiency improvements that compound over time.

Cash Flow and Capital Returns: The Buyback Machine

Adobe's cash flow generation is arguably the most underappreciated part of its financial profile. Here are the key numbers:

- Operating Cash Flow (TTM): $10.03 billion — a record

- Capital Expenditures: just $179 million (Adobe is an asset-light business)

- Free Cash Flow: approximately $9.85 billion

- FCF Yield: roughly 8.5% at the current market cap — extremely high for a tech company

Where does that cash go? Primarily into aggressive share buybacks. Adobe spent $11.28 billion on stock buybacks in FY2025 alone, up from $9.50 billion in FY2024 and $4.40 billion in FY2023. Over the last decade, cumulative buybacks exceed $48 billion.

At current depressed price levels, these buybacks are arguably more accretive than at any point in Adobe's history. The company is retiring shares at a P/E of 17x instead of the 40-50x it has historically traded at. For long-term shareholders, this is a meaningful tailwind.

The AI Question: Threat or Opportunity?

This is the question that has driven Adobe's valuation collapse — and it's genuinely complex.

The bear case is straightforward: generative AI tools are democratizing creativity. Canva (now at over $4 billion in annualized revenue, growing 36% year-over-year) offers an increasingly capable free and low-cost alternative. Midjourney, Runway, and OpenAI's tools can generate professional-grade images and video. Figma dominates collaborative design. If "good enough" AI-generated content replaces the need for expert-level tools, Adobe's premium pricing is at risk.

The bull case centers on Adobe's integration depth and enterprise positioning. Adobe's Firefly AI model is already embedded across Creative Cloud, and the company has adopted an "open platform" strategy — integrating third-party models from Google, OpenAI, Runway, and others directly into its tools. The logic is that while anyone can generate an image, professionals still need Photoshop to refine it, Premiere to edit the video, and Experience Cloud to distribute it at scale. Adobe's workflow integration creates switching costs that standalone AI tools can't replicate.

There's also the Semrush acquisition ($1.9 billion, all cash, expected to close in H1 2026). This deal adds SEO and Generative Engine Optimization (GEO) capabilities to Adobe's Experience Cloud — positioning the company for a world where brands need to be discoverable not just in Google search, but in AI-generated answers from ChatGPT, Gemini, and other large language models. It's a forward-looking strategic move that addresses how marketing itself is being reshaped by AI.

Key Risks to Monitor

No analysis is complete without addressing the risks:

1. AI disruption is real and accelerating. Even if Adobe is well-positioned today, the pace of AI development means the competitive landscape could look very different in 12-18 months. Canva's recent acquisitions in motion graphics and video advertising show it's not standing still.

2. The FTC lawsuit over subscription practices. The Federal Trade Commission sued Adobe in June 2024 over allegedly deceptive subscription cancellation practices. A federal judge rejected Adobe's attempt to dismiss the case in May 2025, and the lawsuit is heading toward trial alongside a separate class action. While the financial impact may be limited (Adobe has stated that early termination fees represent less than 0.5% of revenue), a negative outcome could force changes to Adobe's subscription model and create reputational damage.

3. Valuation compression could persist. The entire SaaS sector is being re-rated as investors question whether traditional software companies can maintain growth in an AI-driven world. Even if Adobe's fundamentals remain strong, the stock may stay cheap if the sector narrative doesn't shift.

4. Execution risk on AI monetization. Adobe needs to prove that AI features can drive tangible revenue growth — not just user engagement. The market needs to see AI contributing meaningfully to ARR growth, not just showing up in marketing materials.

What to Watch on March 12

When Adobe reports Q1 FY2026 earnings after the close on March 12, here are the metrics that matter most:

- Net new ARR: This is the single most important number. Analysts expect approximately $460 million. A beat here would signal that AI fears are overblown; a miss would validate concerns about competitive pressure.

- Digital Media revenue growth: Needs to stay at or above 10% to support the current growth narrative.

- Forward guidance: Any changes to the FY2026 outlook ($25.9–26.1 billion revenue, $23.30–23.50 EPS) will move the stock significantly.

- AI commentary on the earnings call: Investors will be listening for concrete metrics on Firefly adoption, generative credit usage, and AI-driven subscription upgrades.

- Semrush acquisition update: Any timeline clarity on closing and integration plans.

The Bottom Line

Adobe's fundamentals are, by virtually every quantitative metric, at or near their best levels in the company's history. Revenue is growing at double digits, margins are stable and industry-leading, cash flow generation is at record highs, and the balance sheet is clean. The company is buying back shares at an unprecedented pace and at historically cheap valuations.

At the same time, the stock trades at its lowest P/E in a decade, reflecting a market that is deeply skeptical about AI-era software moats. The Burry rumors — unconfirmed as they are — underscore the contrarian nature of owning Adobe right now.

Whether the fundamentals eventually win or the narrative risk materializes is something only time will answer. But the data gives you a foundation for making that judgment yourself.

All fundamental data and charts in this article were generated using Awalyt's fundamental analysis tools. Awalyt provides institutional-grade financial analysis with daily data granularity — including profitability ratios, valuation metrics, growth trends, and more — for investors who want to see beyond the headlines.

Have questions about how to analyze stocks like this? Try it on Awalyt.

Want to test these insights on your own portfolios?

Awalyt is a portfolio analysis platform: backtesting on daily data, fundamental analysis, asset analysis, and AI-powered insights.

Get Started FreeRelated Insights

Nike Stock: Turnaround or Value Trap? What the Data Shows Before Q3 Earnings [March 2026]

14 min read

How to Tell If a Stock Is Overvalued or Undervalued: A Framework with Real Examples [2026]

13 min read

How to Use Historical P/E to Tell If a Stock Is Cheap or Expensive [2026]

10 min read

Why Is My Portfolio Underperforming the S&P 500? [2026]

11 min read

Is Your Portfolio Really Diversified? How to Check [2026]

8 min read

VOO + SMH: More Tech, or Real Diversification? [2026]

10 min read