Core + Satellite Portfolio Strategy: How to Build a Portfolio That Grows AND Protects Your Money [2026]

Most investors build one portfolio and hope for the best. They either go too conservative — low returns, frustrating to watch — or too aggressive, and then panic when the market drops 30%.

There is a better way. And it's called the core + satellite strategy.

It's not new. Institutional investors and pension funds have used it for decades. But most retail investors have never heard of it. In this article, I'll explain what it is, how to build it, and I'll show you real backtest data from both sides so you can see the actual numbers behind the theory.

What Is the Core + Satellite Strategy?

The core + satellite strategy is a portfolio approach where you split your investments into two distinct parts — not two separate accounts, but two logical allocations within the same portfolio.

The core is your foundation. Stable, diversified, low maintenance. It's designed to deliver steady returns while absorbing market shocks without dramatic drawdowns.

The satellite is your growth engine. Higher risk, higher potential returns. It requires more attention and research, but it's where you can meaningfully outperform a simple index strategy.

The idea is that both parts serve a different job. The core protects you when markets get rough. The satellite gives you the upside you're actually looking for. Together, they create a portfolio that is harder to break emotionally — because when your satellite is down, your core is holding steady.

Important disclaimer: The portfolios and assets used in this article are examples chosen to explain the concept. They are not investment recommendations. Before investing, especially in a satellite portfolio, you should conduct your own research and analysis. Past performance does not guarantee future results.

Building the Core Portfolio

The core portfolio should represent around 60 to 70% of your total investments. The goal is not to maximize returns — it's to maximize stability per unit of risk.

Here's what a well-constructed core looks like:

| Asset | Ticker | Allocation | Role |

|---|---|---|---|

| Vanguard Total Stock Market ETF | VTI | 35% | US equity exposure |

| Vanguard Total International Stock ETF | VXUS | 20% | Geographic diversification |

| SPDR Gold Shares | GLD | 20% | Inflation hedge, crisis buffer |

| Vanguard Total Bond Market ETF | BND | 15% | Fixed income stability |

| Vanguard Real Estate ETF | VNQ | 10% | Real estate exposure, income |

This core is intentionally built to cover multiple asset classes and geographies. US stocks, international stocks, gold, bonds, and real estate. When one goes down, the others often cushion the fall.

What "low maintenance" actually means

Low maintenance means you rebalance once a year. You set your target allocation, check it annually, and bring it back in line if one asset class has drifted significantly. That's it. No daily monitoring, no reaction to news.

This discipline is actually where the core delivers its real value — by preventing you from making emotional decisions.

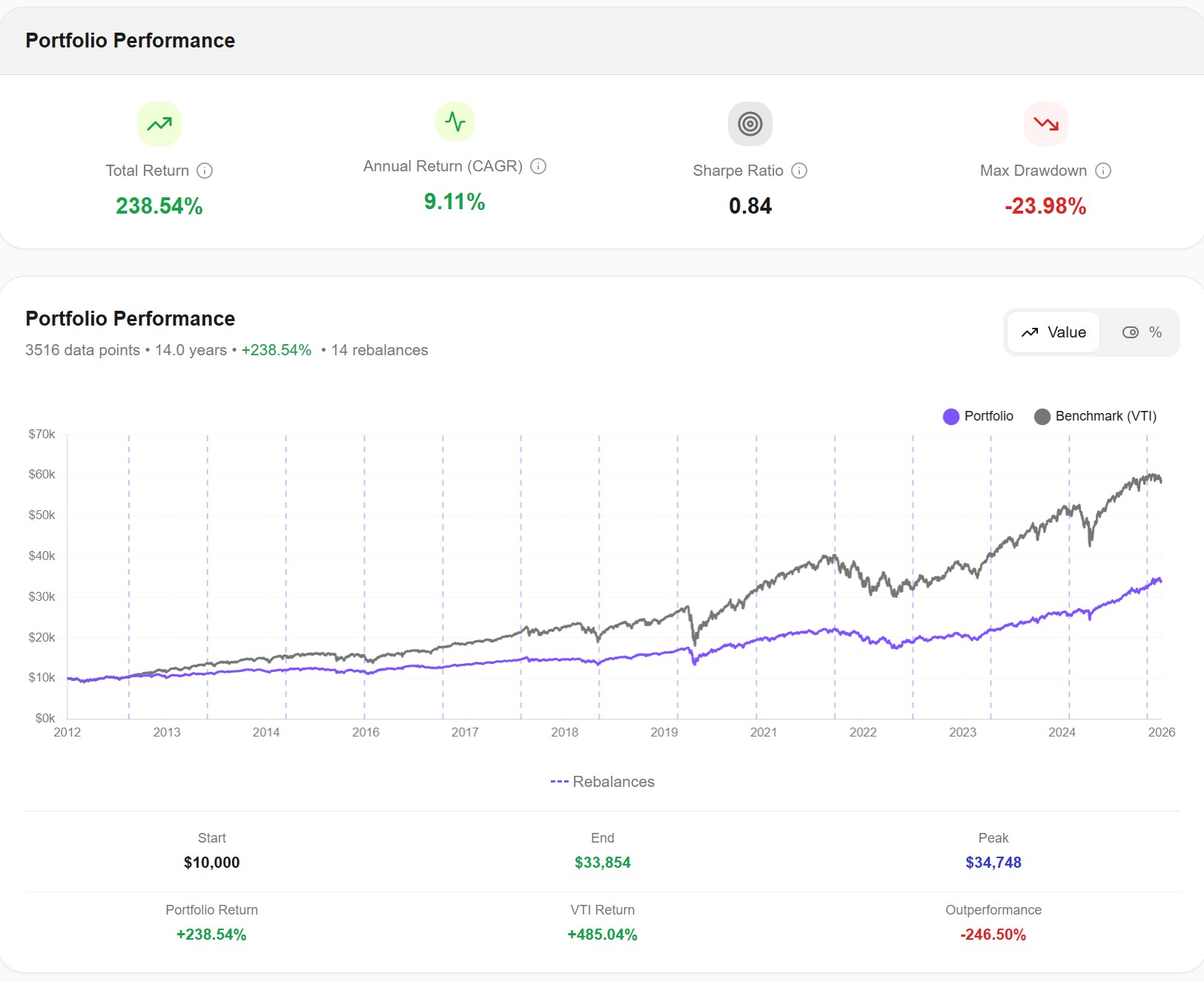

Core Portfolio: What the Backtest Shows

We backtested this core portfolio over 14 years (2012–2026) using daily data. Here is what we found:

| Metric | Core Portfolio | VTI (Benchmark) |

|---|---|---|

| Total Return | +238.54% | +485.04% |

| CAGR | 9.11% | ~15% |

| Sharpe Ratio | 0.84 | — |

| Max Drawdown | -23.98% | ~-36% |

| Volatility | 11.17% | 17.34% |

| Beta | 0.59 | 1.00 |

The core underperforms VTI in raw return. This is expected and by design.

What it gives you in exchange: a max drawdown of -23.98% vs. roughly -36% for VTI, a volatility of 11.17% vs. 17.34%, and a beta of 0.59 — meaning it moves at about half the intensity of the broader market during downturns.

A Sharpe ratio of 0.84 and a Sortino of 1.05 confirm that this portfolio delivers solid risk-adjusted returns. You are not giving up performance arbitrarily — you are trading some upside for significantly less volatility. And that lower volatility is exactly what lets you hold through crises without selling at the bottom.

The right benchmark for the core is not total return — it's stability. Does it hold up in 2020? Does it recover quickly? Does it let you sleep at night? On all three, yes.

Building the Satellite Portfolio

The satellite portfolio represents the remaining 30 to 40% of your investments. This is where you take calculated, research-backed risks in pursuit of higher returns.

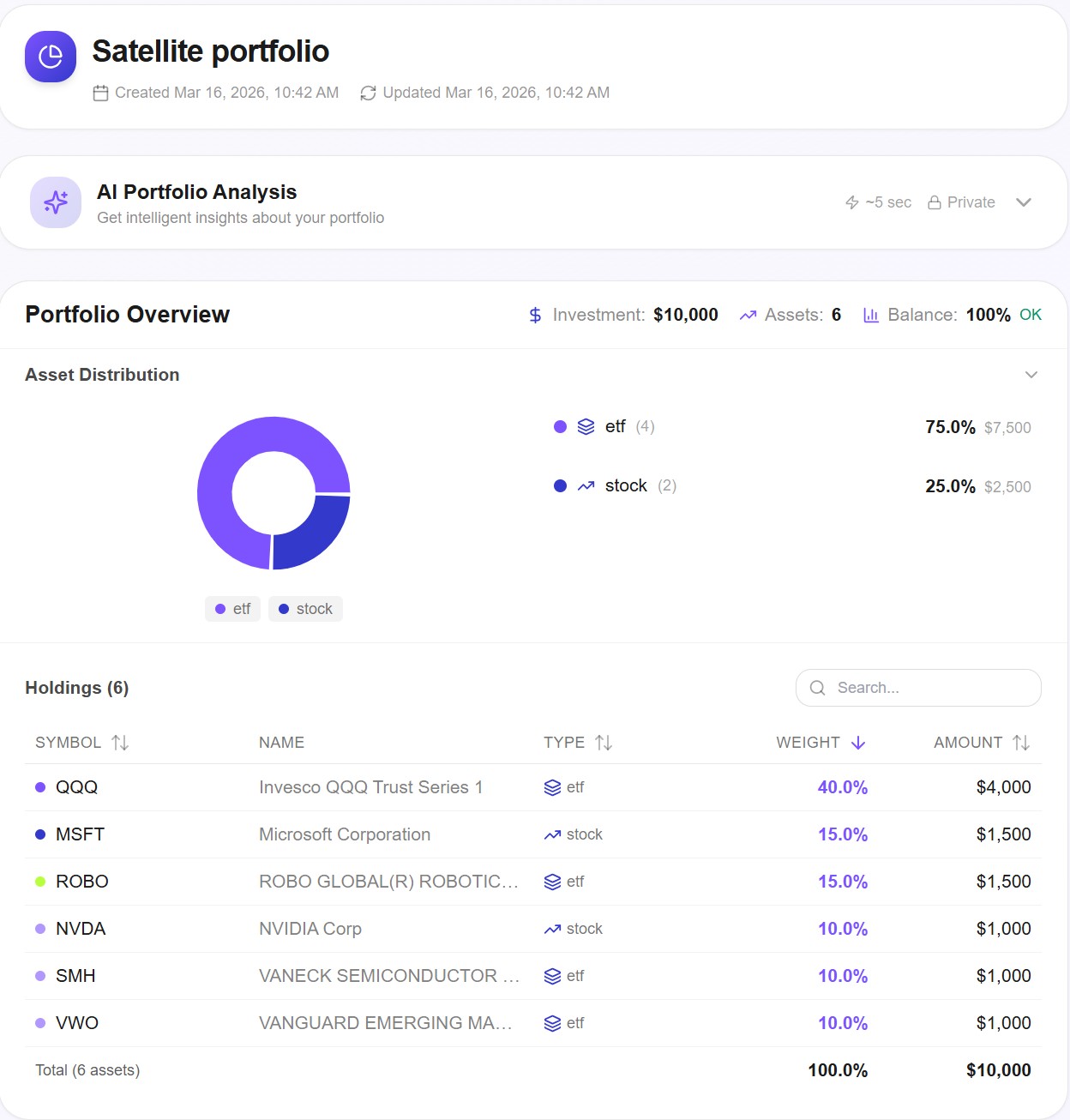

Here's an example satellite portfolio built around growth and emerging technology themes:

| Asset | Ticker | Allocation | Thesis |

|---|---|---|---|

| Invesco QQQ Trust | QQQ | 40% | Nasdaq 100, broad tech and growth |

| Microsoft Corporation | MSFT | 15% | AI infrastructure, cloud dominance |

| ROBO Global Robotics & Automation | ROBO | 15% | Robotics and automation exposure |

| NVIDIA Corporation | NVDA | 10% | AI chips, direct exposure to the AI cycle |

| VanEck Semiconductor ETF | SMH | 10% | Semiconductor sector breadth |

| Vanguard Emerging Markets ETF | VWO | 10% | High-risk geographic diversification |

This satellite is deliberately concentrated in technology, AI, and growth. It's the opposite of the core — higher risk, higher volatility, but with a clear directional thesis.

What the satellite requires from you

Unlike the core, the satellite demands active attention. Before investing in any satellite position — especially individual stocks — you should:

- Analyze company fundamentals (revenue growth, margins, debt, valuation)

- Understand the macro environment (interest rates, sector cycles, geopolitical risks)

- Backtest the strategy to understand historical drawdowns

- Size your positions relative to your total portfolio risk budget

Tools like Awalyt can help you backtest satellite strategies and analyze the fundamentals of individual stocks before you commit capital.

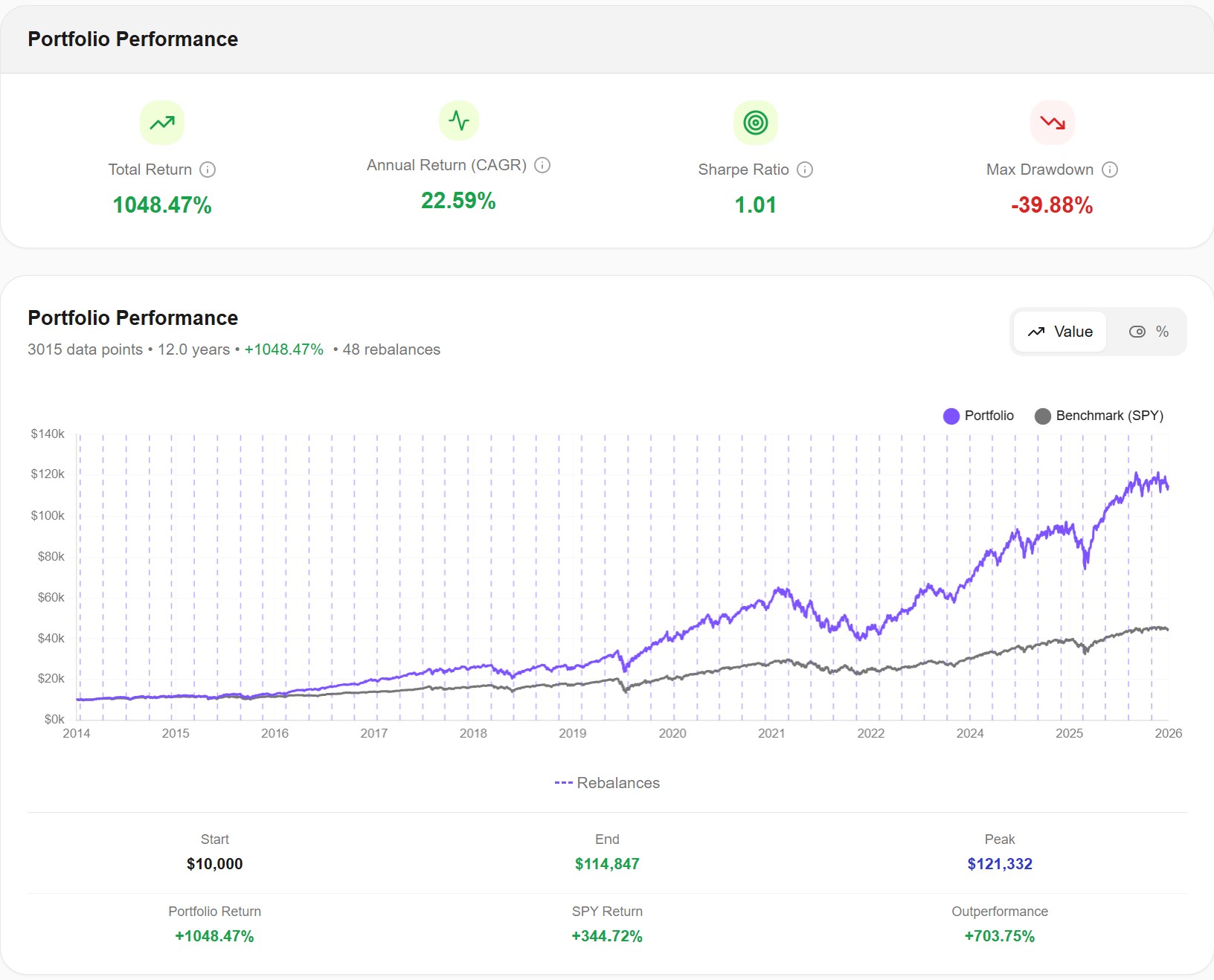

Satellite Portfolio: What the Backtest Shows

We backtested this satellite portfolio over 12 years (2014–2026) using daily data against SPY as benchmark.

| Metric | Satellite Portfolio | SPY (Benchmark) |

|---|---|---|

| Total Return | +1048.47% | +344.72% |

| CAGR | 22.59% | 13.26% |

| Sharpe Ratio | 1.01 | 0.81 |

| Max Drawdown | -39.88% | -33.70% |

| Volatility | 22.87% | 17.34% |

| Beta | 1.21 | 1.00 |

| Alpha | +6.26% | 0.00% |

The satellite crushes SPY in total return — +1048% vs. +344% over 12 years, starting from $10,000. CAGR of 22.59% vs. 13.26%. Alpha of +6.26% per year means this portfolio generated genuine excess return beyond what market exposure alone would explain.

The tradeoff: a max drawdown of -39.88% and a volatility of 22.87%. This is not a comfortable ride. There will be periods where this portfolio drops 30-40%. That is precisely why you do not put 100% of your money here — and why the core exists.

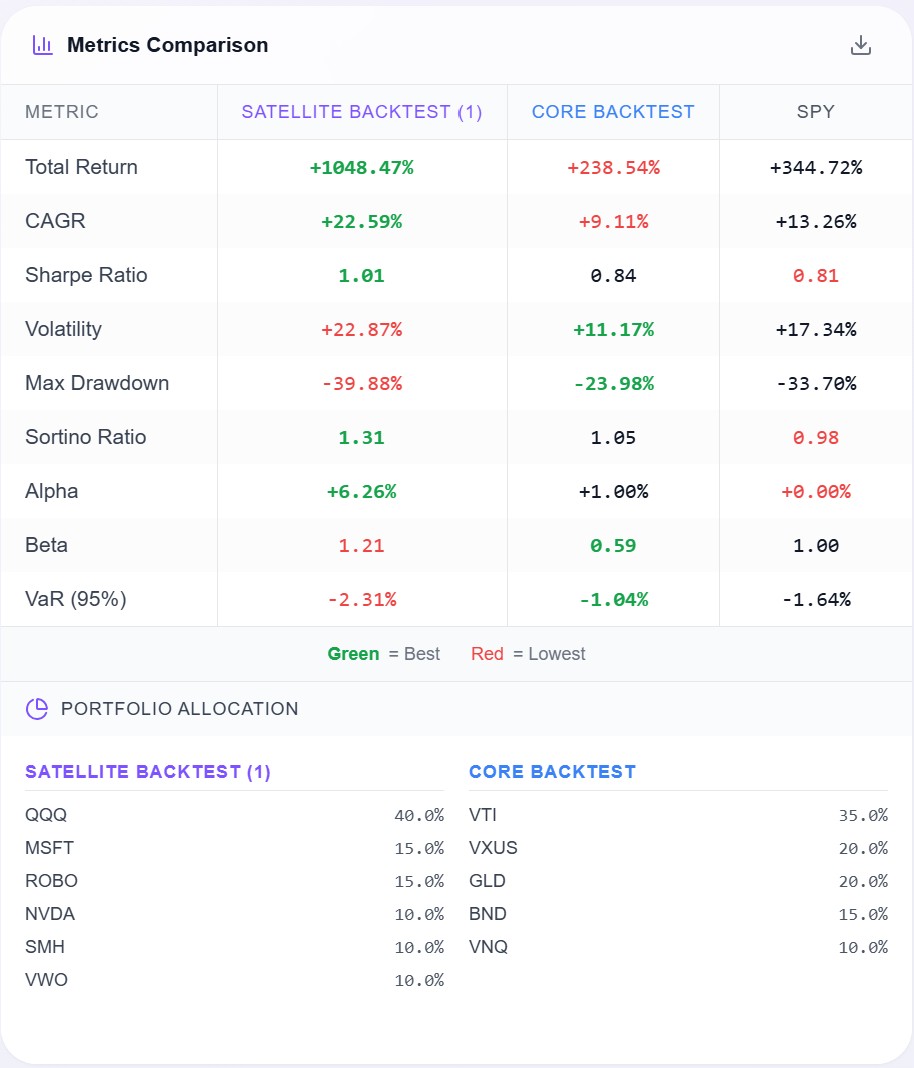

Comparing Core, Satellite, and SPY Side by Side

| Metric | Satellite | Core | SPY |

|---|---|---|---|

| CAGR | +22.59% | 9.11% | 13.26% |

| Sharpe Ratio | 1.01 | 0.84 | 0.81 |

| Volatility | 22.87% | 11.17% | 17.34% |

| Max Drawdown | -39.88% | -23.98% | -33.70% |

| Beta | 1.21 | 0.59 | 1.00 |

| VaR (95%) | -2.31% | -1.04% | -1.64% |

| Alpha | +6.26% | 1.00% | 0.00% |

The picture is clear. The core wins on every risk metric — lower volatility, lower drawdown, lower beta, lower daily VaR. The satellite wins on every return metric — higher CAGR, higher alpha, better Sharpe. SPY sits in the middle and wins at neither.

A combined 65/35 core-satellite allocation would theoretically blend these profiles — capturing most of the satellite's upside while keeping the core's stability as a floor.

How to Size Each Part

The 70/30 or 65/35 split is a starting point, not a rule. How you size each part depends on three things:

Your time horizon. If you're investing for 20+ years, you can tolerate more satellite exposure because you have time to recover from drawdowns. If your horizon is 5 years, the core should dominate.

Your emotional risk tolerance. A -40% drawdown on paper is one thing. Watching your account drop $40,000 when you invested $100,000 is another. Be honest with yourself here. The satellite is not for everyone, and there's nothing wrong with running a 90/10 or even a 100/0 split heavily weighted toward the core.

Your research capacity. The satellite requires real work. If you don't have the time or interest to analyze companies and track macro trends, reduce satellite exposure and rely more on diversified ETFs even within that portion.

When and How to Rebalance

Because core and satellite are part of the same account, rebalancing works as follows:

The core rebalances annually. Pick a date — January 1st works — and bring each asset back to its target weight. Simple, low friction.

The satellite rebalances based on thresholds. If a position grows significantly beyond its target weight, you take partial profits and reallocate. There's no fixed schedule here — it's driven by position drift and your ongoing research.

The important mechanism: if your satellite does very well and grows from 30% to 45% of your total portfolio, you sell the excess and add to the core. This is counterintuitive — you're selling what's winning — but it's the discipline that protects gains and keeps your risk profile in check. You sell because your strategy says so, not because you're afraid.

Common Mistakes to Avoid

Over-complicating the core. The core should have 4 to 6 ETFs maximum. Adding more does not meaningfully improve diversification — it adds noise and makes rebalancing harder.

Not checking correlation between core and satellite. If your core is heavy in US equities (VTI) and your satellite is also heavy in US tech (QQQ, NVDA), you're more correlated than you think. In a US market crash, both sides will fall together. The point of the separation is partly to reduce this correlation.

Treating the satellite like a trading account. The satellite is not for short-term trades. It's for medium to long-term theses that you've researched and backtested. Frequent trading in the satellite generates friction, taxes, and emotional noise.

Rebalancing emotionally. The worst time to sell satellite positions is when they're down. Rebalance on schedule or at preset thresholds — not in reaction to market news.

How to Test Your Strategy Before Committing Capital

One of the most important steps before implementing any portfolio strategy is backtesting it with real historical data. This is where most retail investors skip a critical step.

For the core portfolio, backtesting tells you how it behaved during the 2020 COVID crash, the 2022 rate hike cycle, and other stress periods. It shows you the actual drawdown depths — not approximations — and how quickly the portfolio recovered.

For the satellite portfolio, backtesting combined with fundamental analysis gives you confidence in your position sizing. You can see whether your thesis has historical support before risking real capital.

Awalyt offers backtesting for both portfolio types with daily precision data, plus a Fundamentals module for analyzing individual stock positions in the satellite. You can test your core allocation in minutes and run the comparison against any benchmark you choose.

Final Thoughts

The core + satellite strategy is not a shortcut. It requires you to be intentional about two different jobs your money needs to do — stability and growth — and to build each part correctly.

The data we've shown here is illustrative. Your actual allocation, asset selection, and performance will differ based on your choices, timing, and market conditions. The assets in these example portfolios were chosen to explain the concept, not as specific recommendations.

What the data does confirm is the logic behind the separation: the core absorbs shocks, the satellite generates alpha, and together they create a portfolio with a better risk-adjusted profile than either part alone.

Start by deciding your split. Then backtest your core. Then research your satellite positions one by one. Build with data, not with gut feeling.

Want to test these insights on your own portfolios?

Awalyt is a portfolio analysis platform: backtesting on daily data, fundamental analysis, asset analysis, and AI-powered insights.

Get Started FreePortfolios mentioned in this article

Related Insights

How to Build a Core ETF Portfolio: A 5-Step Framework

12 min read

Backtesting a Portfolio: 6 Common Mistakes and How to Avoid Them [2026]

11 min read

Why Is My Portfolio Underperforming the S&P 500? [2026]

11 min read

How to Check ETF Overlap for Free (VOO vs QQQ) [2026]

9 min read

How to Run a Free DCA Backtest (VOO Example) [2026]

8 min read

10 Years of $300/Month DCA: What Happened on VOO, QQQ, AAPL, and 7 Other Popular Assets [2026]

11 min read